Independent financial advice: 7 Powerful Benefits 2025

Why Independent Financial Advice is Your Gateway to Unbiased Investment Guidance

Independent financial advice is professional financial guidance provided by advisers who aren’t tied to specific financial institutions or pressured to sell proprietary products. These advisers can recommend solutions from the entire market and are compensated through transparent fees rather than hidden commissions.

Key characteristics of independent financial advice:

– No product bias – Advisers can recommend any suitable product from any provider

– Transparent fees – You pay the adviser directly, not through hidden commissions

– Fiduciary duty – Legal obligation to act in your best interests

– Whole-of-market access – Access to all available financial products and services

– Regulatory oversight – Licensed and monitored by financial authorities

The demand for truly independent guidance has never been higher. With over 5,000 financial advisers operating in the UK alone and growing networks like PEAK Financial Group managing $15 billion in assets across Canada, more professionals are breaking free from institutional constraints to offer unbiased advice.

Yet finding genuine independence isn’t always straightforward. Many advisers claim to be “independent” while still operating under restrictive dealer agreements or receiving incentives that influence their recommendations.

As Ray Gettins, Director of United Advisor Group, I’ve spent years helping exceptional advisors transition to truly independent financial advice models that prioritize client outcomes over institutional profits. Our structure is designed by advisors for advisors, providing the flexibility and collaboration needed to serve clients without conflicts of interest.

Why This Guide Matters

The financial advice industry is riddled with conflicts of interest that can cost you thousands of dollars over time. When your adviser is incentivized to sell specific products or meet sales quotas, their recommendations may not align with your best interests.

Our research shows that only 16% of financial advice firms in the UK would take on clients with less than £100,000 to invest, highlighting how traditional models often exclude smaller investors. Meanwhile, truly independent advisers focus on providing whole-of-market solutions regardless of your investment size.

This guide provides the peace of mind that comes from understanding exactly what independence means, how to verify it, and how to work with truly independent professionals who put your interests first.

What Is Independent Financial Advice?

Definition of Independent Financial Advice

Think of independent financial advice as having a friend who knows the entire financial world and has no reason to steer you wrong. It’s professional guidance from advisers who aren’t tied to any bank, insurance company, or investment firm. They don’t get paid extra for pushing certain products, and they’re not under pressure to meet sales targets.

The beauty of true independence lies in the freedom it creates. When your adviser isn’t beholden to any particular company, they can search the entire marketplace to find what actually works best for your situation.

Different countries have their own rules about what “independent” means, but the heart remains the same everywhere. In the UK, independent financial advisers were officially recognized back in 1988 to separate them from salespeople tied to single companies. Since 2013, UK rules have been even stricter – these advisers must tell you exactly what you’ll pay upfront and can’t take hidden commissions.

The scope of independent financial advice covers your entire financial life. We’re talking retirement planning, investment strategies, tax efficiency, insurance needs, and estate planning. Unlike restricted advisers who can only pick from a limited menu of products, independent advisers have access to everything that’s legally available in their country.

Independent Financial Advice vs. Bank or Tied Advice

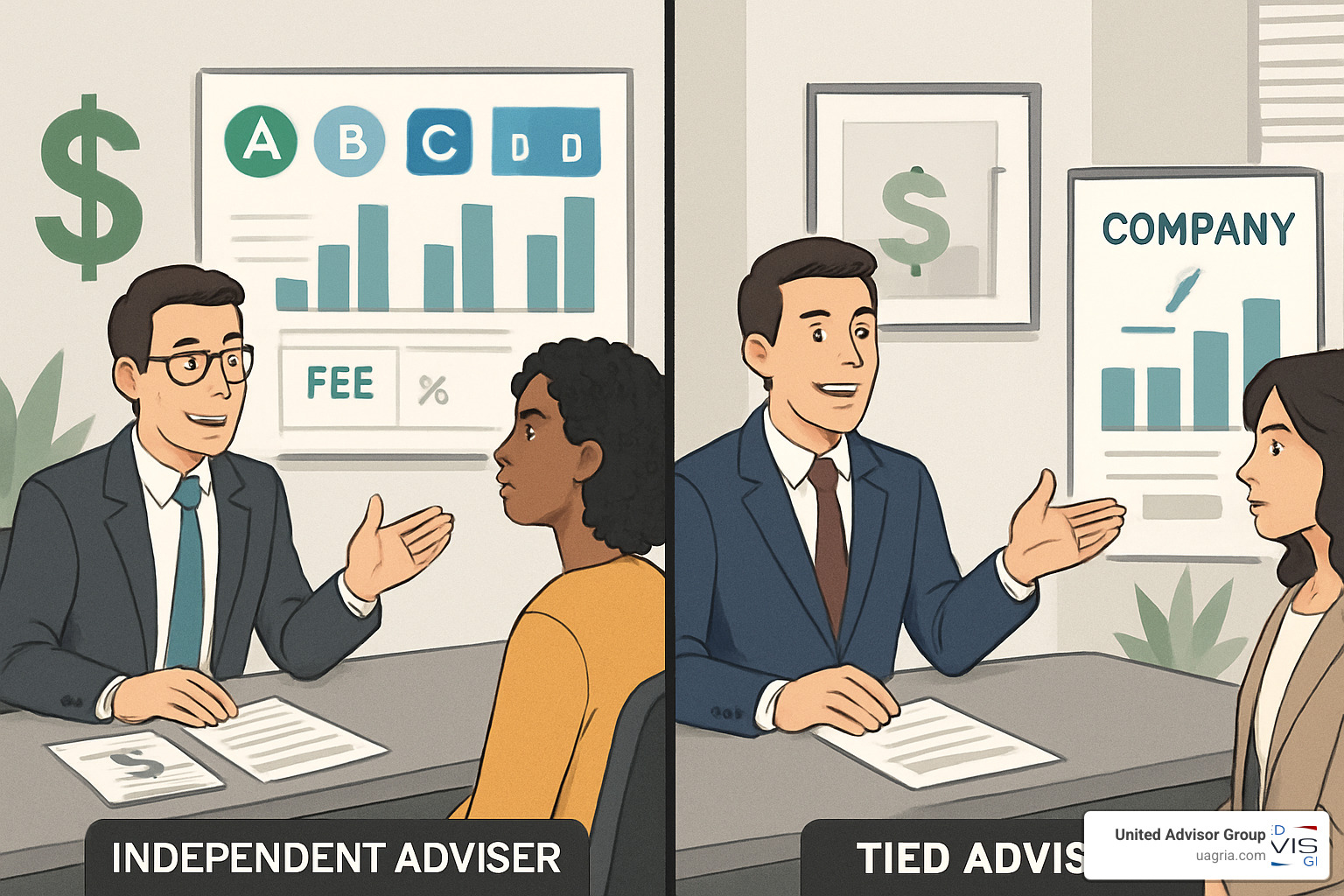

The difference between independent financial advice and what you get from your bank is like the difference between a neutral referee and a player on the opposing team.

Bank advisers are employees first and advisers second. They have sales targets to hit, bonuses tied to specific products, and a boss who expects them to generate revenue for the bank.

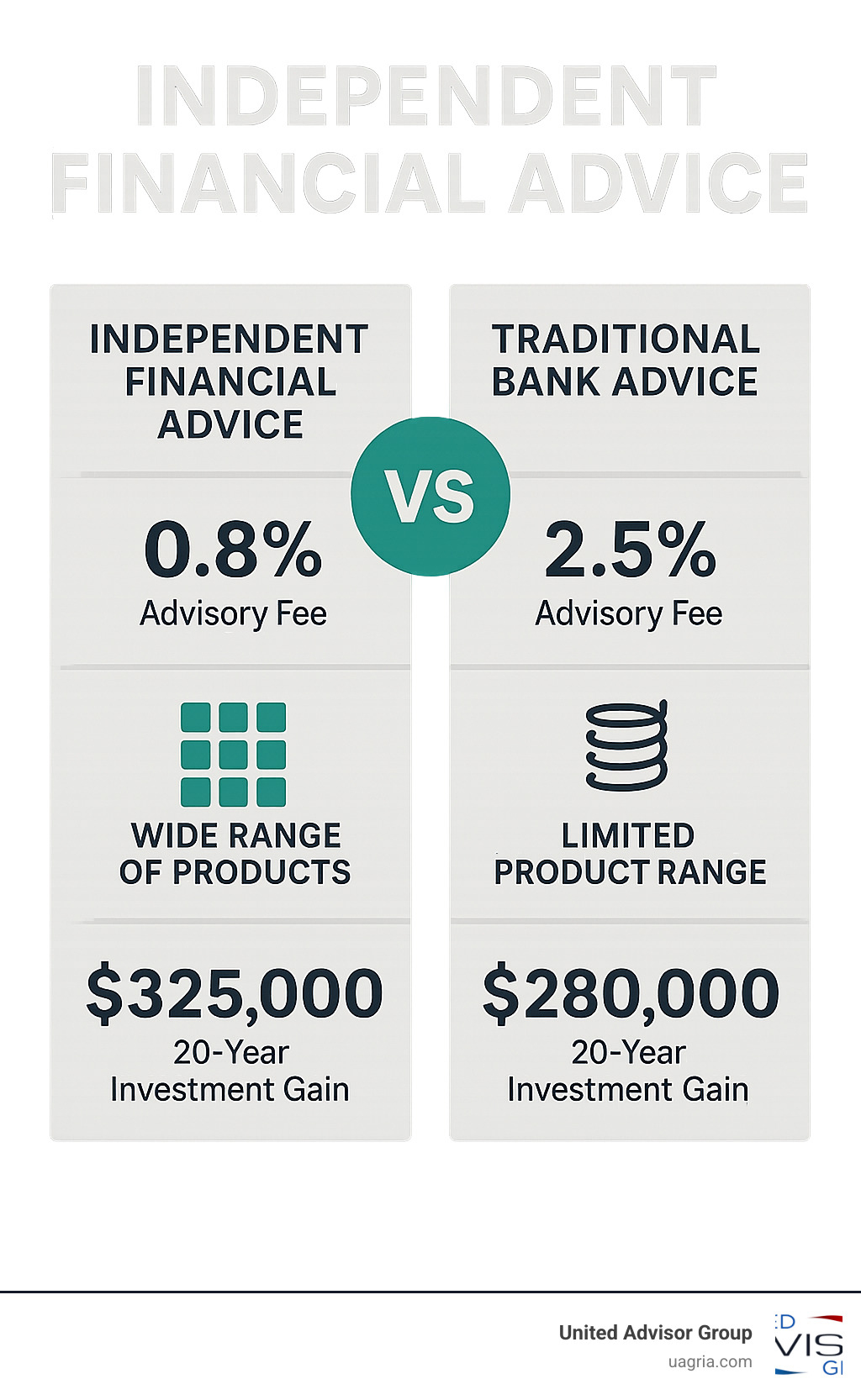

Let me give you a real example. A bank adviser might recommend their institution’s managed investment fund that charges 2.5% per year. An independent adviser, looking at the same situation, might find an identical fund from another provider charging just 0.8% annually. On a $100,000 investment over 20 years, that difference costs you more than $45,000 in extra fees.

Independent advisers flip this equation entirely. You pay them directly through transparent fees, which means they have zero incentive to recommend expensive products. Their success depends entirely on your satisfaction and results, not on hitting sales quotas or pushing proprietary products.

When you work with an independent adviser, you’re hiring someone whose job is to be on your side. When you work with a tied adviser, you’re essentially asking someone whose paycheck depends on selling you things to give you unbiased advice about whether you should buy those things.

Benefits & Limitations of Going Independent

Key Advantages You’ll Enjoy

When you choose independent financial advice, you’re essentially hiring someone whose success depends entirely on helping you succeed. This ethical alignment creates a professional relationship where your adviser genuinely wants what’s best for you because that’s literally how they get paid.

When your adviser doesn’t get kickbacks from mutual fund companies or insurance providers, they have zero reason to recommend anything other than what truly serves your needs. This client-first approach means you’ll get comprehensive recommendations that draw from the entire universe of financial products, not just whatever happens to be sitting on your adviser’s company shelf.

The freedom this creates is remarkable. Need a low-cost index fund? Your independent adviser will find the best one available, even if it means lower fees for them. Looking for specialized insurance or alternative investments? They’ll search the whole market to find exactly what fits your situation.

You’ll also enjoy custom fee structures that actually make sense. Instead of wondering what hidden costs are buried in your investments, you’ll know exactly what you’re paying and why. Many independent advisers offer flexible arrangements—maybe you need just one hourly consultation to review your 401(k), or perhaps you want ongoing management with transparent asset-based fees.

Studies consistently show that when advisers operate without sales quotas or pressure to push house products, their clients achieve better long-term outcomes. When someone’s only job is to give you good advice, that’s exactly what you tend to get.

Potential Drawbacks to Consider

Cost transparency can feel like a cold splash of water when you’re used to “free” bank advice. When an independent adviser quotes you £200 per hour for a consultation, it might seem expensive compared to walking into your bank branch where advice appears to cost nothing.

Of course, that bank advice isn’t really free—you’re paying through higher product fees and commissions that are cleverly hidden from view. But psychologically, writing a check directly to your adviser can feel more painful than paying invisible costs over time.

Adviser availability presents another real challenge. Since truly independent advisers represent a smaller slice of the financial advice world, you might find fewer options in your area. This is especially true if you live in a rural area where your choices might be limited to the local bank branch or a tied agent who primarily sells insurance products.

You’ll also face a due-diligence burden that some people find overwhelming. With independent advice, you need to verify credentials, understand fee structures, and make sure your adviser is properly licensed and insured.

Many independent advisers also maintain minimum asset thresholds—often £100,000 or more—which can exclude smaller investors who might benefit most from unbiased guidance.

But here’s the thing: these limitations often fade once you experience the difference that truly independent guidance makes. While independent advice might require more upfront effort and cost transparency, it typically delivers far better value over the long term.

How to Verify & Choose an Independent Financial Adviser

Finding a truly independent adviser isn’t as simple as taking someone’s word for it. Many advisers claim independence while still operating under restrictive agreements or receiving hidden incentives. The verification process requires detective work, but it’s worth the effort to ensure you’re getting genuinely unbiased independent financial advice.

Step-by-Step Verification Process

Start with the official regulatory registers in your jurisdiction. In the UK, check the Financial Services Register. Canadians should search the National Registration Search, while New Zealand residents can use the FSPR and Australians should check ASIC’s register. These databases tell you if an adviser is properly licensed and whether they’ve faced any disciplinary action.

Look beyond just basic licensing to understand their qualifications. In the UK, advisers must hold at least Level 4 qualifications—equivalent to first-year university level—and maintain a Statement of Professional Standing with 35 hours of annual training. Chartered advisers have even higher Level 6 qualifications, equivalent to first-class honors degree level.

Check disciplinary history through multiple channels including IIROC, CSA, or MFDA depending on your location. Even search the Better Business Bureau and provincial authorities. A clean regulatory record doesn’t guarantee quality advice, but disciplinary actions are definite red flags.

Now comes the crucial part—verifying their independence claims. Ask these specific questions: Do you receive any payments from product providers? Are you tied to any dealer or institution? Can you recommend products from any provider? Do you have sales targets or quotas? True independence means “no” to all payments, ties, and targets.

Professional associations provide an extra layer of verification. The Certified Independent Financial Advisers Association (CIFAA) in Australia requires members to have no ownership links with financial institutions and prohibits commission payments. The Independent Financial Brokers (IFB) in Canada offers similar verification for truly independent professionals.

Choosing the Best Fit for Your Needs

Once you’ve verified independence, finding the right fit becomes more personal. Personal chemistry matters more than many people realize—you’ll be sharing intimate details about your finances, goals, and fears. The best adviser for you is someone who listens well, explains things clearly, and makes you feel comfortable asking questions.

Most advisers offer free initial consultations. Use these meetings like job interviews in reverse—you’re interviewing them. Pay attention to how they communicate. Do they use jargon or explain things in plain English? Do they seem genuinely interested in your situation?

Service scope should align with your needs. Some independent advisers specialize in investment management, others focus on comprehensive financial planning, and some excel at specific areas like retirement planning or tax strategies.

Fee models vary significantly among independent advisers. Hourly fees typically range from £200-500+ per hour, while asset-based fees usually fall between 0.5-2% annually. Fixed-fee planning might cost £1,000-5,000 for comprehensive plans. Choose a model that makes sense for your budget and the complexity of your situation.

Consider their typical client profile too. Some advisers specialize in high-net-worth clients with complex needs, while others focus on middle-income families building wealth. You’ll receive better service from an adviser whose typical client looks like you in terms of assets, income, and financial goals.

More info about selecting advisors

Working With an Independent Adviser: Process, Costs & Ethics

Typical Engagement Timeline

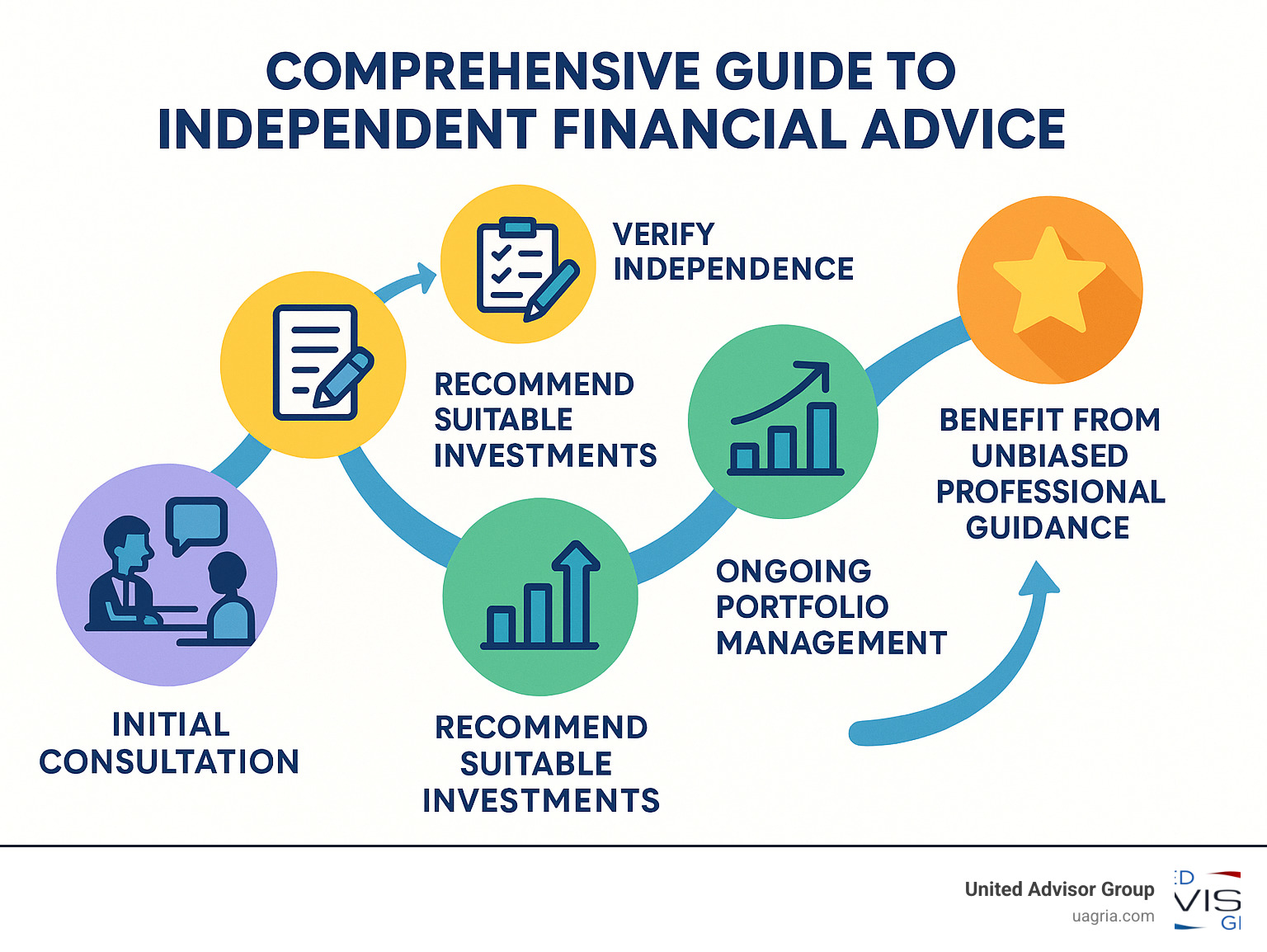

When you decide to work with an independent financial advice professional, you’re starting on a journey that’s quite different from walking into a bank and being sold a product. The process is more thoughtful, more thorough, and ultimately more rewarding.

Your journey begins with what we call the fact-find phase—though it’s really more like a financial heart-to-heart. Your adviser will want to know everything about your money situation, from your current savings and debts to your dreams for the future. Good advisers know that numbers only tell part of your story.

Goal-setting comes next, and this is where things get exciting. You’ll work together to turn your vague hopes (“I want to retire comfortably”) into specific, achievable targets (“I need $60,000 annual income starting at age 65”). This clarity makes all the difference in creating a plan that actually works.

The strategy phase produces written recommendations that explain exactly what your adviser suggests and why. This isn’t a sales pitch—it’s a detailed roadmap showing how each recommendation fits your situation.

Implementation can happen all at once or be spread over time, depending on your comfort level and the complexity of your plan. Your adviser will guide you through account openings, transfers, and any paperwork involved. The beauty of independence is that they can recommend the best providers for each piece of your plan.

Ongoing monitoring keeps your plan on track as life changes. Most advisers recommend annual reviews, but major life events—marriage, divorce, job changes, or inheritance—might trigger additional check-ins.

Understanding Fees & Their Impact

Let’s talk about money—specifically, what you’ll pay for truly independent financial advice. The good news is that you’ll know exactly what you’re paying, unlike the hidden fees buried in traditional financial products.

Hourly fees typically run from $200-500+ per hour, depending on your adviser’s experience and your location. This might seem steep, but consider that you’re paying for unbiased expertise that could save you thousands in unsuitable product fees.

Asset-based fees usually range from 0.5-2% annually of the money your adviser manages. While this creates an ongoing cost, it also means your adviser’s success is tied to your portfolio’s performance. They make more money when your investments do well, which aligns their interests with yours.

Fixed-fee planning might cost $1,000-5,000+ for a comprehensive financial plan. This works well if you want detailed guidance but prefer to implement recommendations yourself.

The real impact of transparent fees goes beyond the numbers on your statement. When your adviser isn’t paid more for recommending expensive products, they can focus on finding the most cost-effective solutions for your needs. This freedom from product bias often saves you far more than the advisory fees cost.

Ensuring Your Values Are Reflected

Your money should reflect who you are, not just what you want to earn. Modern independent financial advice recognizes that true financial success means aligning your investments with your personal values and beliefs.

Values-based investing has evolved far beyond simple exclusion screens. Whether you care deeply about environmental sustainability, social justice, or specific ethical considerations, independent advisers can build portfolios that honor your principles while pursuing your financial goals.

ESG screening (Environmental, Social, and Governance) has become remarkably sophisticated. You can exclude specific industries like tobacco or weapons manufacturing, focus on companies with strong diversity practices, or prioritize businesses leading the fight against climate change.

Personal alignment extends to the advisory relationship itself. Independent advisers can adapt their communication style, meeting frequency, and service approach to match your preferences. This personalization is possible because independent advisers aren’t constrained by institutional procedures or one-size-fits-all service models.

The services independent advisers provide span the full range of financial planning—retirement strategies, tax optimization, insurance analysis, and estate planning. They can also incorporate specialized areas like education funding or business succession planning.

Understanding Independent Fiduciary & Virtual Family Office Roles

Learn More IFB CE Central Accredited online education by IFB

Frequently Asked Questions about Independent Financial Advice

What services do independent advisers provide?

Independent financial advice covers every aspect of your financial life, from basic investment guidance to complex wealth management strategies. Think of independent advisers as financial generalists who can address whatever challenges you’re facing—whether that’s planning for retirement, managing taxes, or protecting your family with the right insurance.

Investment management forms the core of most advisory relationships. Your adviser might build and monitor a diversified portfolio for you, or they might provide recommendations that you implement yourself. The key difference is that they can choose from thousands of investment options rather than being limited to their employer’s products.

Retirement planning often becomes the central focus as you approach your later working years. Independent advisers help you steer pension options, plan tax-efficient withdrawal strategies, and coordinate multiple retirement accounts.

Tax planning weaves through everything else they do. Every investment decision, pension contribution, and insurance purchase has tax implications. Independent advisers can optimize these decisions because they’re not constrained by institutional limitations or product quotas.

Business owners often find independent advisers particularly valuable for navigating the complexities of corporate finances, succession planning, and personal wealth extraction strategies.

How can I confirm my adviser is truly independent?

The most important question to ask is simple: “Do you receive any payments from the companies whose products you recommend?” True independence means the answer is always no. Your adviser should be paid exclusively through the fees you pay directly—no commissions, bonuses, or incentives from product providers.

Check their licensing status through official regulatory databases. These public registers show exactly what your adviser is licensed to do and whether they’ve faced any disciplinary actions. It takes just a few minutes and gives you peace of mind about their credentials.

Ask about their institutional relationships. Some advisers claim to be independent while actually working for companies that manufacture financial products. Truly independent advisers either operate their own practices or work with platforms that don’t have proprietary products to sell.

Professional association membership can provide additional verification. Organizations like the Independent Financial Brokers (IFB) in Canada maintain strict independence requirements for their members.

Pay attention to how they describe their services. Independent advisers talk about finding the best solutions for your needs. Tied advisers often focus on their company’s products and services.

What questions should I ask before signing an agreement?

Start with the basics: “What are your qualifications and how long have you been providing independent financial advice?” You want someone with proper credentials and enough experience to handle your specific situation.

Get complete clarity on costs before moving forward. Ask for written disclosure of all fees, including management charges, transaction costs, and any additional services that might cost extra. Independent advisers should provide this information willingly and clearly.

Discuss their investment philosophy and approach to risk management. You need to understand how they make decisions and whether their style matches your comfort level.

Ask about communication expectations. “How often will we meet? What reports will I receive? How quickly do you respond to emails or calls?” Establishing these expectations upfront prevents frustration later.

Finally, inquire about their complaints procedure. While you hope never to need it, understanding how disputes are resolved shows their professionalism and commitment to client service.

Conclusion & Next Steps

You now have the roadmap to finding truly independent financial advice—the kind that puts your interests first, every single time. This isn’t just about finding someone to manage your money. It’s about partnering with a professional who has the freedom to recommend what’s genuinely best for your unique situation.

The difference is profound. While tied advisers are constrained by institutional products and sales targets, independent advisers can search the entire market for solutions that fit your needs perfectly. They’re paid through transparent fees rather than hidden commissions, which means their success depends on your success—not on selling you expensive products.

This empowered decision-making starts with understanding what true independence looks like. Remember the key markers: no proprietary products to push, no sales quotas to meet, and no hidden payments from product providers. When you find an adviser who meets these criteria, you’ve found someone who can focus entirely on your financial wellbeing.

The verification process we’ve outlined isn’t complicated, but it is essential. Check those regulatory registers, ask about fee structures, and don’t be shy about questioning their independence claims. A truly independent adviser will welcome these questions—they’re proud of their unbiased approach.

At United Advisor Group, we’ve seen how independence transforms outcomes for both advisers and their clients. Our structure eliminates the conflicts that plague traditional models. We don’t manufacture products, set sales targets, or create compliance burdens that distract from client service.

Instead, we’ve built a collaborative environment where advisers have complete autonomy to recommend any solution from any provider. This isn’t just better for clients; it’s what attracted exceptional advisers to our platform in the first place.

Your financial future deserves this level of care and attention. The peace of mind that comes from knowing your adviser has no hidden agenda is invaluable. Whether you’re planning for retirement, building wealth, or navigating a major life change, independent advice ensures you’re getting recommendations based on what’s right for you—not what’s profitable for someone else.

Take the next step today. Use the tools and knowledge from this guide to find an independent adviser who matches your needs and values. Ask the tough questions, verify their credentials, and don’t settle for anything less than true independence.

Choose an adviser who puts your interests first, and you’ll have a partner who’s genuinely invested in your long-term success.

Registered Investment Advisor: Enhancing Client Relationships