Retirement and Tax Planning: 10 Powerful Tips for 2025 Success

Why Smart Tax Planning Can Make or Break Your Retirement

Retirement and tax planning is crucial because taxes can dramatically reduce your retirement income if not managed properly. Here’s what you need to know:

Key Tax-Efficient Retirement Strategies:

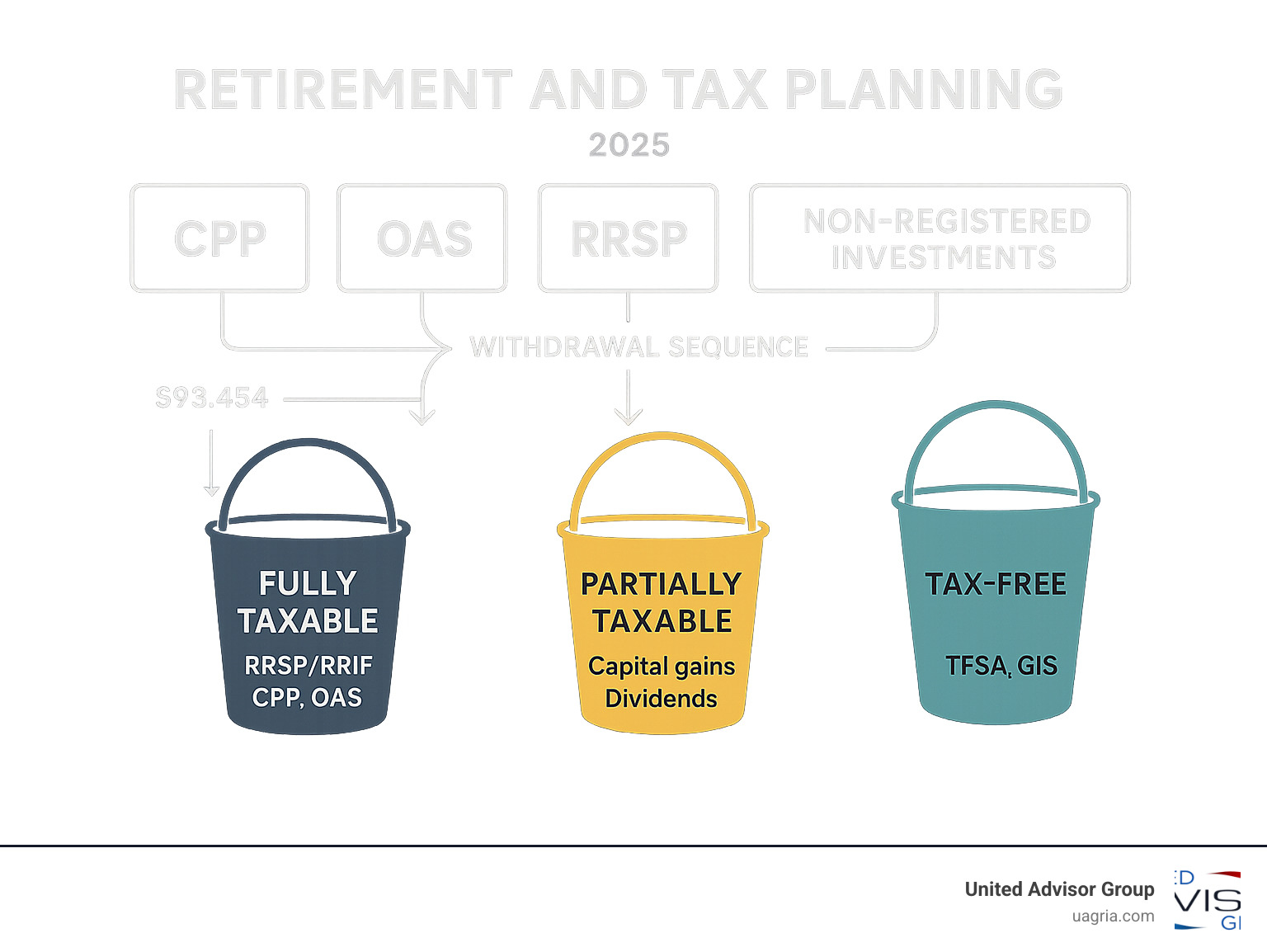

– Withdraw in order: RRIF minimums first, then non-registered accounts, then TFSA last

– Split pension income: Up to 50% with your spouse to lower combined tax burden

– Manage government benefits: Keep net income below $93,454 to avoid OAS clawback

– Use tax-free accounts: TFSA withdrawals don’t affect your tax bracket or benefits

– Time your benefits: Defer CPP/QPP and OAS to increase payments and manage brackets

Research shows that 74% of Canadians worry about having enough income in retirement, yet 53% don’t realize their CPP benefits are taxable.

The reality is simple: it’s not just what you save, it’s what you keep after taxes. With OAS clawbacks starting at $93,454 and top marginal rates exceeding 50% in some provinces, poor tax planning can cost you tens of thousands annually.

Smart withdrawal sequencing alone can save retirees significant money. For example, taking a $10,000 RRSP withdrawal in a lower-income year versus a higher-income year can save over $505 in federal tax alone.

I’m Ray Gettins, and through my work with independent financial advisors, I’ve seen how proper retirement and tax planning transforms clients’ financial futures. My experience helping advisors steer complex tax strategies has shown me that the best retirement plans always integrate tax efficiency from day one.

Why Taxes Matter as Much as Returns

When we think about retirement planning, we often focus on investment returns and savings rates. But taxes can erode your retirement income just as much as poor investment performance.

Consider this scenario: Two retirees each have $500,000 saved. The first withdraws $50,000 annually without tax planning, paying 31.48% on excess income above $93,132 in Ontario. The second uses strategic withdrawal sequencing and income splitting, staying in lower brackets. Over 20 years, the tax-savvy retiree could save over $74,000 in combined taxes.

That’s why we believe retirement and tax planning should be viewed as two sides of the same coin, not separate financial goals.

How Retirement Income Is Taxed in Canada

Understanding how your retirement income gets taxed is crucial for effective retirement and tax planning. Canadian retirement income isn’t all taxed the same way – think of it like a traffic light system.

Your fully taxable retirement income includes RRSP and RRIF withdrawals, Canada Pension Plan (CPP) or Quebec Pension Plan (QPP) benefits, Old Age Security (OAS), employer pension plans, and employment income. Interest from non-registered investments also falls into this category.

Partially taxable income gets more favorable treatment. Capital gains only see 50% included in your taxable income. Eligible Canadian dividends get grossed up by 38% but benefit from the dividend tax credit, often resulting in lower effective tax rates.

Tax-free income includes TFSA withdrawals, which won’t cost you a dime in taxes and won’t affect your government benefits. The Guaranteed Income Supplement (GIS) is also tax-free.

Here’s how the major retirement accounts stack up:

| Account Type | Contributions | Growth | Withdrawals | Impact on Benefits |

|---|---|---|---|---|

| RRSP/RRIF | Tax-deductible | Tax-deferred | Fully taxable | Increases net income |

| TFSA | After-tax | Tax-free | Tax-free | No impact |

| Non-registered | After-tax | Taxable annually | Only gains taxable | Depends on income type |

Government Benefits & Clawbacks

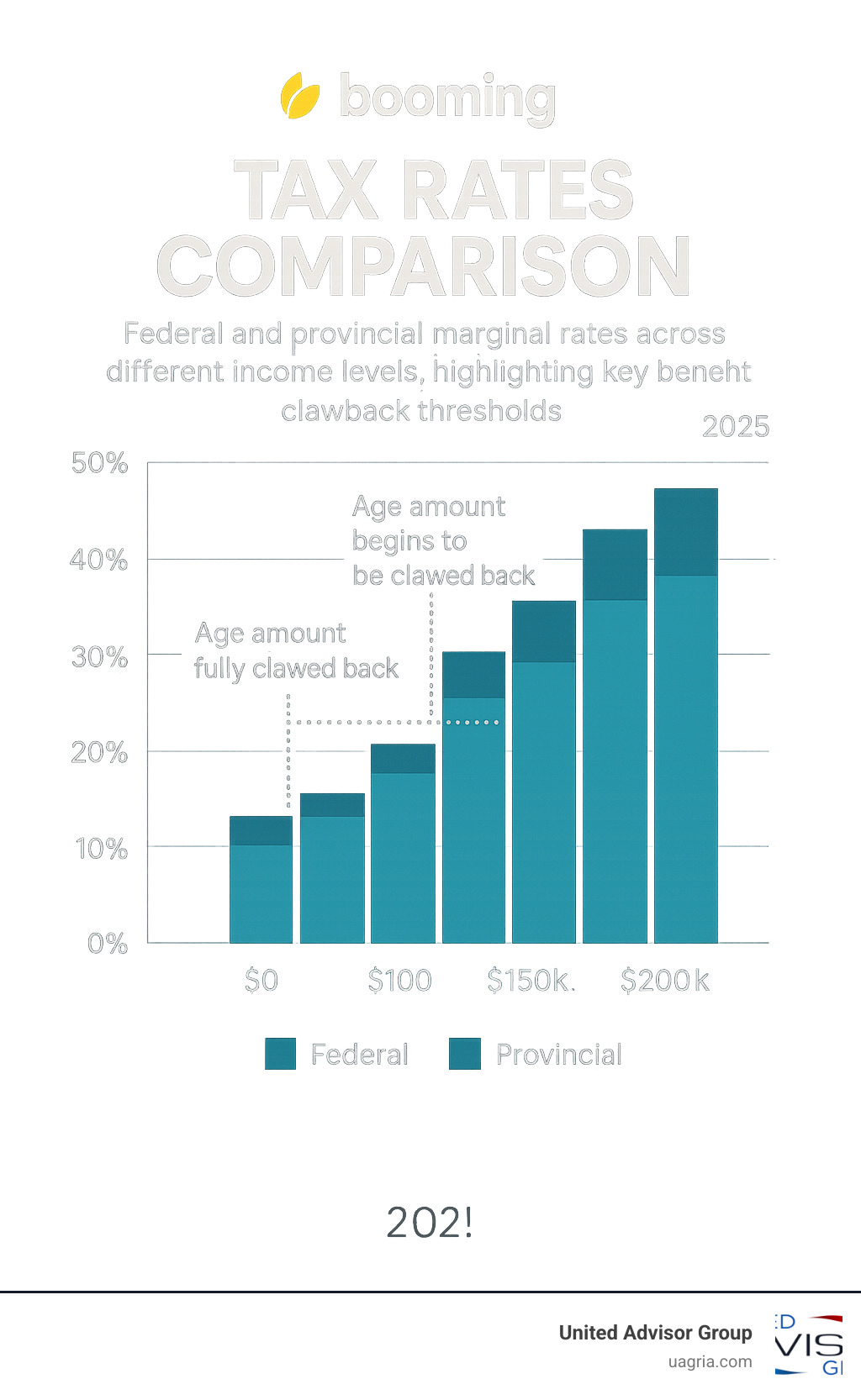

The Old Age Security recovery tax is the major clawback to watch. For 2025, your OAS benefits start getting clawed back when your net income hits $93,454. The government takes back 15 cents of every dollar above that threshold.

The maximum monthly OAS benefit is $727.67 for folks aged 65-74 and $800.44 for those 75 and older. If your net income exceeds $148,451 (or $153,771 if you’re 75+), you lose your entire OAS benefit – up to $9,605 annually.

The OAS pension recovery tax is based on net income (line 23600) on your tax return, including employment income, pensions, RRSP withdrawals, and investment income.

The Age Amount credit provides up to $9,028 in tax relief for 2025, but starts disappearing when your net income exceeds $45,522.

Non-Registered Investment Taxation

Capital gains get favorable treatment – only 50% of your realized gains count as taxable income. This makes them particularly attractive for staying below benefit clawback thresholds.

Dividend income from eligible Canadian dividends benefits from the gross-up and credit system, often resulting in lower effective tax rates. However, that $10,000 dividend gets grossed up to $13,800 for tax purposes.

Interest income gets taxed at your full marginal rate, making interest-bearing investments less appealing in non-registered accounts during retirement.

Retirement and Tax Planning Account Strategies

Smart retirement and tax planning isn’t about picking one perfect account – it’s about creating “tax diversification.” This gives you options to control how much tax you pay each year in retirement.

RRSP and RRIF accounts are your tax-deferred workhorses. Every dollar gives you an immediate tax break, but you’ll pay full taxes on withdrawal. The secret is timing these withdrawals for when they’ll hurt the least.

TFSA accounts are the Swiss Army knife of retirement planning. Since withdrawals don’t count as income, they won’t push you into higher tax brackets or trigger benefit clawbacks.

Non-registered accounts give you the most control. You can choose when to realize capital gains, and you only pay tax on 50% of those gains.

For a complete overview of available deductions and credits, the CRA’s guide on Tax deductions, credits and expenses is an excellent resource. For advanced strategies, explore Open up Tax Savings with Financial Planning: IRC 1202 Tips.

Converting RRSPs to RRIFs Wisely

Minimum withdrawals start at 5.28% of your account value at age 71. But if your spouse is younger, you can use their age for the calculation, significantly reducing your required withdrawals.

Using a younger spouse’s age can drop your minimum withdrawal from 5.28% to 4.00%. On a $500,000 RRIF, that’s $6,400 less you’re forced to withdraw – potentially $2,000 less in taxes.

Timing your conversion doesn’t have to wait until December. If you’re 65 or older and want to start pension income splitting, converting early lets you begin splitting RRIF income right away.

Using TFSAs for Tax-Free Cash Flow

TFSA withdrawals are completely invisible to the tax system. Need $15,000 for a new roof? Take it from your TFSA and it won’t increase your net income or affect your benefits.

TFSA contribution room keeps growing even in retirement. For 2025, you can contribute $7,000, and withdrawn amounts can be re-contributed the following year.

Leveraging Spousal RRSPs & FHSA

Spousal RRSPs help balance retirement income between spouses. Just remember the three-year attribution rule – withdrawals within three years of contribution are taxed back to the contributor.

The First Home Savings Account (FHSA) can be useful for retirees planning to downsize. If you haven’t owned a home in four years, you might qualify as a first-time buyer again, providing up to $40,000 in tax-advantaged savings per person.

Sequencing Withdrawals & Income-Splitting Tactics for Tax Savings

The order in which you withdraw from different accounts can significantly impact your lifetime tax bill. Smart sequencing is at the heart of effective retirement and tax planning.

Withdrawal Sequence & the Primary Goal of Retirement and Tax Planning

The primary goal is to smooth your taxable income over time, avoiding spikes that trigger higher tax brackets or benefit clawbacks.

Here’s the optimal withdrawal order: Start with RRIF minimums since you have no choice. Next, tap non-registered accounts where you can harvest capital gains. Then consider additional RRIF withdrawals to fill lower tax brackets. Save your TFSA for last – these assets are too valuable to touch unless necessary.

In years when your income is naturally lower, consider taking larger RRIF withdrawals to fill up those lower brackets. When income is higher, rely more on capital gains and TFSA withdrawals.

For personalized guidance, our Independent Financial Advice can help you model different scenarios.

Pension Income Splitting & Spousal Loan Strategies

Pension income splitting allows couples to split up to 50% of eligible pension income. This includes registered pension payments, RRIF withdrawals after age 65, and CPP benefits through pension sharing.

Imagine a couple where one spouse has $80,000 in pension income while the other has $20,000. By splitting $30,000, they move to a balanced $50,000/$50,000 split, potentially saving thousands in taxes annually.

Spousal loan strategies work by having the higher-income spouse lend money to the lower-income spouse at the CRA prescribed rate. Investment returns above that rate get taxed in the lower-income spouse’s hands.

Working After Retirement or Abroad

Working while collecting pensions can push you into higher brackets, but you can continue contributing to CPP for post-retirement benefits. The key is managing your total income picture.

Living abroad part-time brings considerations about non-resident withholding tax rates and tax treaty benefits. Understanding these rules before extended absences can save considerable money.

Advanced Tools: Spousal Loans, Trusts, Annuities & Cross-Border Issues

When your retirement and tax planning needs become complex, advanced strategies can provide additional tax savings and estate planning benefits.

Family trusts remain valuable when adult children are in lower tax brackets, though recent changes have made them more complex to implement.

Prescribed rate loans allow investment growth above the prescribed rate to be taxed in lower-income beneficiaries’ hands.

Annuities can transform how your income is taxed. Life annuities provide guaranteed income with a portion of each payment considered tax-free return of capital. Prescribed annuities maximize the return of capital treatment for non-registered funds.

Our Custom Investment Solutions can help evaluate whether these strategies align with your goals.

Estate Planning & Minimizing Taxes at Death

RRIF rollover strategies allow the entire balance to roll over tax-free to your spouse, deferring taxes until your spouse withdraws the funds.

Charitable bequests can provide powerful tax relief at death. Leaving a portion of your RRIF to charity generates a donation receipt that can offset the taxable income created.

Life insurance funded during your lifetime can cover estate taxes, particularly valuable when you have significant RRIF assets that will create large tax liabilities.

Adapting the Plan Over Time

Tax legislation changes can significantly impact your strategy. The recent increase in capital gains inclusion rate is a perfect example affecting investment strategy and estate planning.

Market volatility early in retirement can derail plans. You might need to adjust withdrawal strategies to avoid depleting assets too quickly.

We recommend scenario testing your retirement plan regularly. What happens if markets drop 30%? What if inflation averages 4% instead of 2%? Testing these scenarios helps ensure your plan remains robust.

Frequently Asked Questions about Retirement and Tax Planning

How do minimum RRIF withdrawals affect my tax bill?

RRIF minimum withdrawals are fully taxable income that gets added to everything else you’re earning. The withdrawal percentages start at 5.28% when you’re 71, climbing to 20% by age 94.

If your spouse is younger, you can use their age to calculate minimums, potentially saving thousands. Another approach is taking your minimum early in January, then investing excess into your TFSA if you have contribution room.

Consider taking more than the minimum in early retirement years when income might be lower. Smoothing withdrawals over time often results in paying less total tax.

What’s the optimal age to start CPP/QPP and OAS from a tax standpoint?

Starting CPP early at 60 reduces benefits by up to 36%, while delaying until 70 increases them by up to 42%. The tax implications can tip the scales significantly.

If you’re still working with significant income in your early 60s, taking CPP early might push you into higher brackets. If you’re in a lower bracket and can invest those payments at good returns, starting early might make sense.

OAS deferral up to age 70 provides a 36% permanent increase. This makes sense if you’re facing clawbacks anyway – defer the benefit and receive more later.

Can I keep contributing to my TFSA after 71?

Absolutely! There’s no age limit for TFSA contributions. With the 2025 limit at $7,000, you can continue building tax-free wealth well into your 80s and beyond.

TFSA withdrawals are completely invisible to the tax system – they don’t push you into higher brackets or trigger benefit clawbacks. For estate planning, TFSAs can transfer tax-free to a surviving spouse.

Conclusion

Retirement and tax planning isn’t something you set and forget – it requires regular attention. The strategies we’ve explored can potentially save you tens of thousands of dollars over your retirement years while giving you confidence in your financial future.

Tax diversification is just as crucial as investment diversification. Having money spread across different “tax buckets” gives you flexibility to adapt when life throws curveballs.

Strategic withdrawal sequencing – taking RRIF minimums first, then using non-registered accounts, and saving your TFSA for last – can significantly boost your after-tax income.

Managing your net income to stay below key thresholds like the $93,454 OAS clawback limit can be worth thousands annually.

At United Advisor Group, we’ve seen how proper planning transforms our clients’ retirement experience. Our independent approach means we focus on strategies that work for your unique situation, not selling products.

Every retiree’s situation is different. Your health, family circumstances, and retirement dreams are uniquely yours. That’s why cookie-cutter advice often falls short.

For those in the Cincinnati area, our Wealth Management Services Designed for Cincinnati Locals can help you implement these strategies. But regardless of location, the principles remain the same.

Your goal isn’t just accumulating money – it’s creating a tax-efficient income stream that lets you live the retirement you’ve imagined while preserving something meaningful for those you care about.

The best time to start optimizing your retirement tax strategy was yesterday. The second-best time is today.