Why Managed Wealth Solutions Are Changing Modern Wealth Management

Managed wealth solutions bring every major part of your financial life—investments, planning, taxes, estate strategy, and risk management—into one coordinated plan. Instead of judging success by portfolio returns alone, this approach measures whether you’re on track for the goals that matter most.

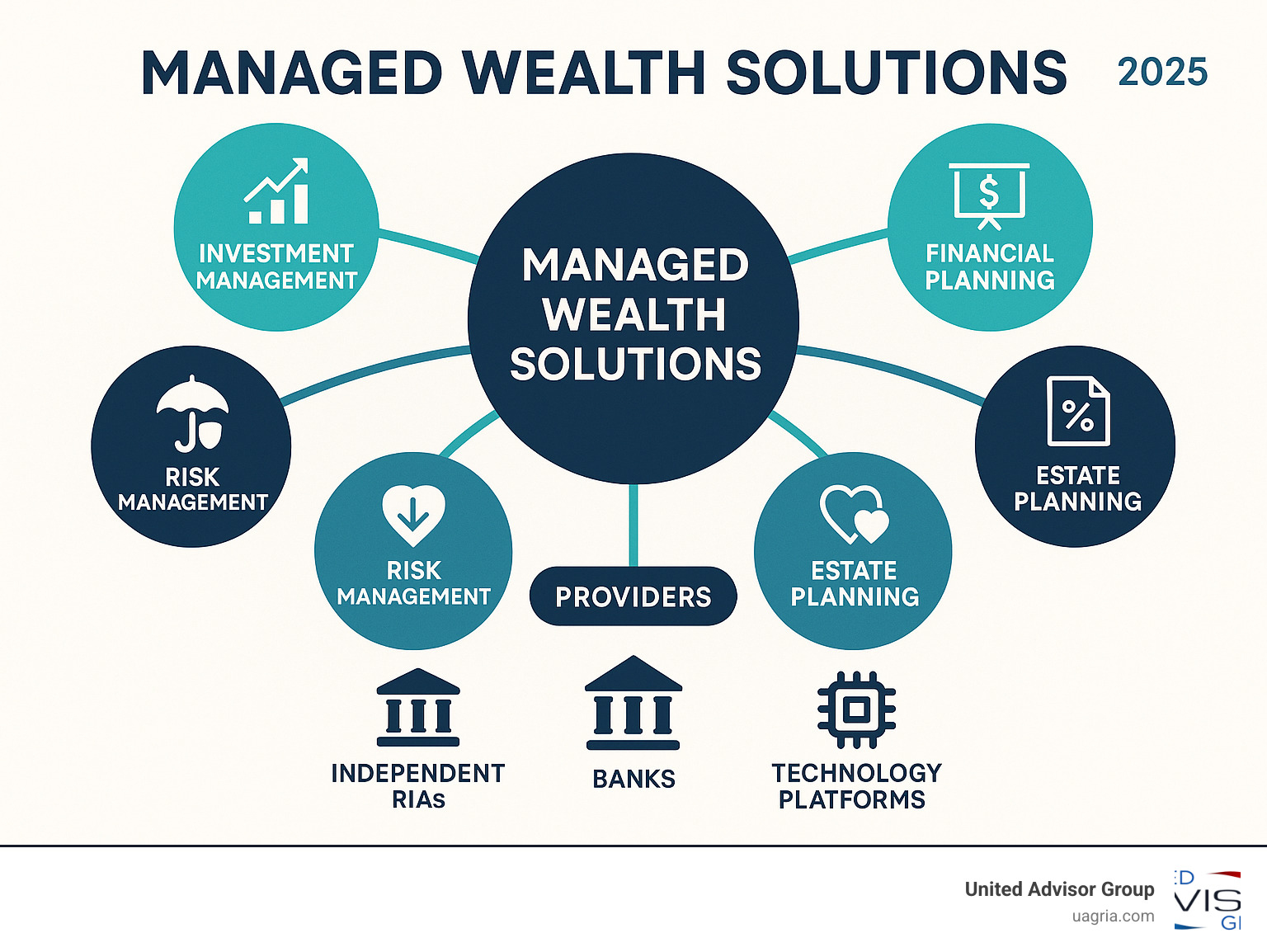

Key Components of Managed Wealth Solutions:

– Investment Management – Professional portfolio construction and monitoring

– Financial Planning – Goal-based roadmaps for retirement, education, and big life events

– Tax Optimization – Techniques such as tax-loss harvesting and smart asset location

– Estate Planning – Wills, trusts, and legacy strategies

– Risk Management – Insurance coordination and asset protection

– Ongoing Monitoring – Regular reviews that adjust as your life changes

The wealth-management profession is entering an Era of Independence: more advisors are leaving traditional broker-dealer models so they can recommend the very best solutions—without product quotas or conflicting commissions. Fee-based, open-architecture platforms let advisors focus squarely on client outcomes.

I’m Ray Gettins, Director at United Advisor Group. We built our practice on that founding idea: when advisors are free from restrictive compliance mandates, they can collaborate, customize, and deliver better results for every client.

What Are Managed Wealth Solutions?

Think of managed wealth solutions as the difference between having a family doctor versus just seeing a specialist when something hurts. Traditional investment management focuses on one thing—your portfolio. Managed wealth solutions look at your entire financial health.

Here’s what makes this approach special: it’s built around a holistic strategy that treats all aspects of your financial life as connected pieces of the same puzzle. Your investment decisions impact your taxes. Your tax planning affects your estate strategy. Your estate plan influences your insurance needs. Everything works together.

The magic happens through integrated planning. Instead of having separate professionals handling your investments, taxes, estate planning, and insurance (who may never talk to each other), managed wealth solutions coordinate all these services under one roof.

But perhaps most importantly, providers of managed wealth solutions typically operate under a fiduciary duty. This means they’re legally required to put your interests first—not just recommend something that’s “suitable” for you.

| Traditional Investment Management | Managed Wealth Solutions |

|---|---|

| Focus on portfolio performance | Holistic financial planning |

| Product-driven recommendations | Goals-based strategies |

| Suitability standard | Fiduciary standard |

| Transactional relationships | Ongoing partnerships |

| Limited scope of services | Comprehensive planning |

| Commission-based compensation | Fee-based transparency |

Managed Wealth Solutions vs Traditional Investment Management

The difference between these two approaches is dramatic. Traditional investment management is like having a really good mechanic who only changes your oil—they do that one thing well, but your car needs more than oil changes to run smoothly.

Managed wealth solutions expand this relationship significantly. Your advisor becomes intimately familiar with your complete financial picture. They know about your kids’ college plans, your parents’ long-term care needs, your business succession goals, and even your charitable interests.

This comprehensive approach allows for much more sophisticated client segmentation. A 35-year-old tech entrepreneur with stock options gets completely different strategies than a 60-year-old doctor preparing for retirement, even if they have similar net worth and risk tolerance.

Personalization at the Core

Real personalization goes way beyond those standard risk questionnaires. Goals-based planning starts with understanding what you’re actually trying to accomplish with your wealth.

Risk profiling in managed wealth solutions considers both your ability to take risk and your comfort with it. You might be able to handle significant portfolio volatility based on your income and time horizon, but if market swings keep you awake at night, that emotional reality becomes part of your financial plan.

More info about custom investment solutions

Core Services in a Modern Managed Wealth Solution

When you work with managed wealth solutions, you’re not just getting an investment manager—you’re getting a complete financial team that actually talks to each other. The magic happens in the integration. Your tax strategy influences your investment decisions. Your estate plan shapes your insurance needs. Your retirement goals drive your cash flow planning.

Comprehensive Financial Planning

Think of comprehensive financial planning as creating a GPS for your financial journey. Modern financial planning starts with cash-flow modeling—understanding exactly how money moves through your life.

Life-stage mapping recognizes that your financial needs change dramatically as you move through different phases. A 30-year-old focused on buying a home has different priorities than a 50-year-old planning for retirement.

The best plans also include scenario analysis. What happens if you lose your job? What if the market crashes right before you retire? These “what if” exercises help you prepare for life’s curveballs.

More info about retirement and tax planning

Investment Management & Portfolio Design

Investment management within managed wealth solutions goes way beyond picking stocks and bonds. Asset allocation forms the foundation—determining the right mix of investments based on your goals, timeline, and comfort with risk.

Rebalancing isn’t just about maintaining your target allocation. Smart rebalancing considers tax implications, cash flow needs, and market opportunities. Sometimes the best move is to not rebalance if it would trigger unnecessary taxes.

Advanced strategies like direct indexing are becoming more accessible. Instead of owning a mutual fund, you own the individual stocks. This gives you much more control over taxes and allows for personalized screening based on your values.

Tax Optimization & Wealth Preservation

Tax optimization can be more valuable than picking great investments. A mediocre investment in the right tax wrapper often beats a great investment that’s tax-inefficient.

Tax-loss harvesting systematically captures losses to offset gains throughout the year. Done properly, this strategy can save significant money annually—money that compounds over decades.

Estate freezes and charitable trusts help high-net-worth families transfer wealth efficiently. These aren’t just for the ultra-wealthy anymore. Many middle-class families benefit from basic estate planning techniques.

Estate & Legacy Planning

Estate planning within managed wealth solutions goes far beyond basic wills and trusts. Modern estate planning includes wills and trusts, but also considers family dynamics, tax efficiency, and philanthropic goals.

For business owners, succession planning becomes critical. How do you transfer ownership while maintaining family harmony? How do you minimize taxes while ensuring the business continues to thrive?

Insurance & Risk Management

Insurance within managed wealth solutions isn’t about selling you products you don’t need. It’s about identifying risks that could derail your financial plan and addressing them efficiently.

Life and disability coverage protects your family’s financial security. Liability shields protect the wealth you’ve worked so hard to build. An umbrella policy costs a few hundred dollars annually but can protect millions in assets.

More info about independent financial advice

Choosing the Right Managed Wealth Solution Provider

Finding the right provider for managed wealth solutions can feel overwhelming. The good news? Once you know what to look for, the choice becomes much clearer. Think of it like choosing a doctor—you want someone with the right credentials, a clean track record, and an approach that fits your needs.

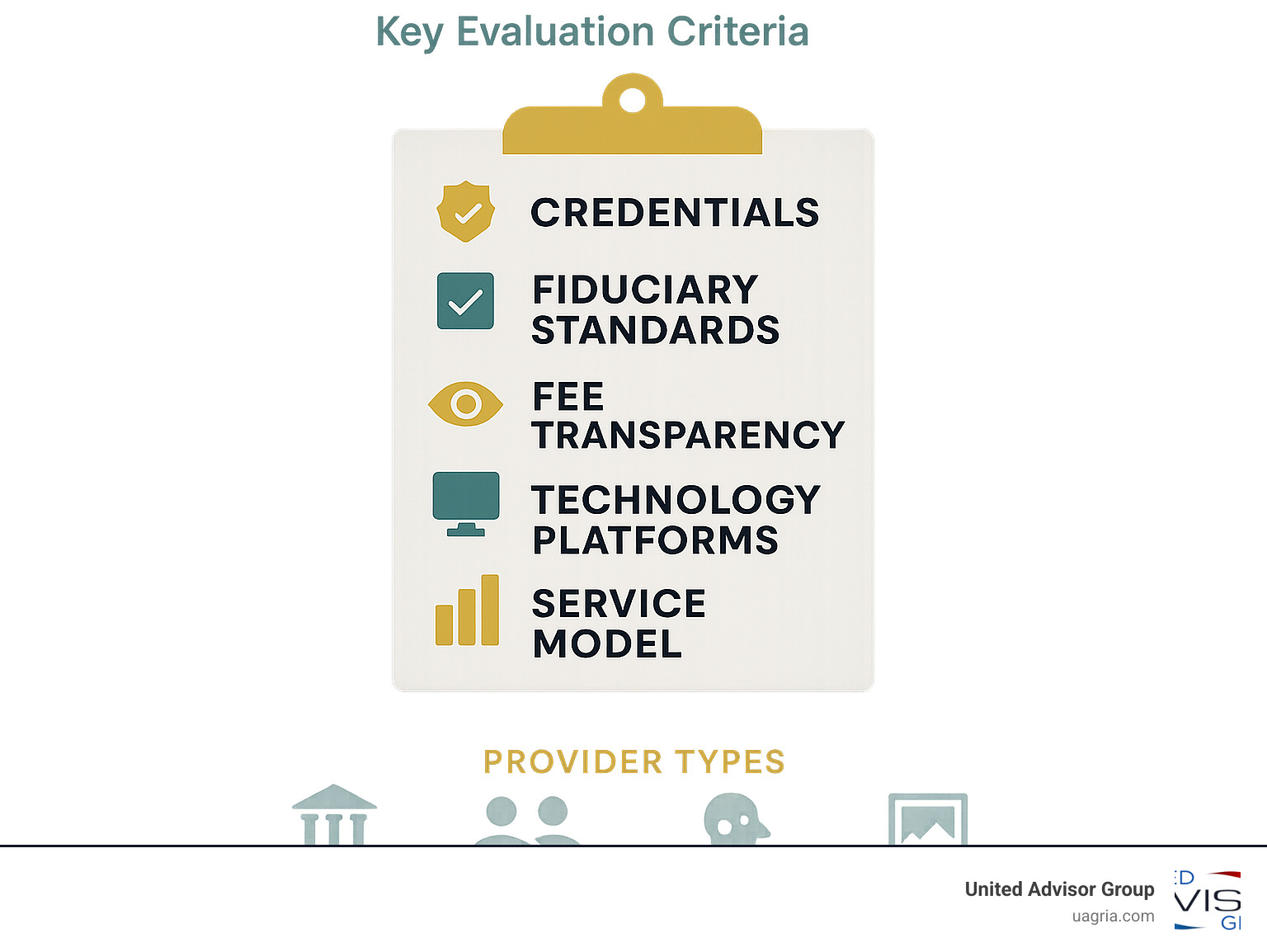

Key Evaluation Metrics

The best managed wealth solutions providers share certain characteristics that you can evaluate before making your decision.

Track record and credentials matter more than fancy marketing materials. Look for advisors with relevant certifications like CFP (Certified Financial Planner), CFA (Chartered Financial Analyst), or ChFC (Chartered Financial Consultant). Check their regulatory record through FINRA’s BrokerCheck or the SEC’s Investment Adviser Public Disclosure database.

Service model alignment is crucial. Some advisors focus exclusively on high-net-worth clients with $10 million or more in assets. Others serve a broader range of clients. Make sure you’re not trying to squeeze into a service model that doesn’t fit your situation.

Net Promoter Score (NPS) has become the gold standard for measuring client satisfaction in wealth management. This metric asks: “How likely are you to recommend this advisor to a friend?” Scores above 50 are considered excellent, and the best providers often score in the 70s or 80s.

Technology and reporting capabilities separate modern providers from those stuck in the past. Your provider should offer robust online portals with real-time account access, integrated reporting across all your accounts, and mobile capabilities.

Latest research on NPS benchmarks

Provider Categories Explained

Understanding the different types of managed wealth solutions providers helps you make an informed choice.

Independent RIAs (Registered Investment Advisors) often represent the gold standard for comprehensive wealth management. These advisors operate under strict fiduciary standards and typically offer fee-based advice without the conflicts that come from selling proprietary products.

Banks and private banks offer the stability and resources of large institutions. They provide comprehensive services and have the financial backing to weather market storms. However, they may have conflicts of interest due to pressure to sell proprietary products.

Robo-advisors use technology to provide automated portfolio management at very low costs. They’re efficient for basic investment management but typically can’t provide the comprehensive planning and personal guidance that comes with full-service providers.

Family offices cater to ultra-high-net-worth families and often provide services that go beyond traditional wealth management. They typically require significant assets—often $25 million or more—to access their services.

Questions to Ask Before Signing

The right questions can reveal everything you need to know about a potential managed wealth solutions provider.

Fee structure transparency should be your first priority. Ask: “What are all the fees I’ll pay, and exactly how are they calculated?” The best providers give you a clear, written breakdown of all costs.

Custody and safety of your assets is non-negotiable. Ask: “Where exactly are my assets held, and what protections exist?” Your money should be held at a qualified custodian with SIPC protection.

Reporting and communication expectations need to be clear upfront. Ask: “How often will we meet, and what reports will I receive?” At minimum, expect quarterly reports and online access to real-time account information.

Conflict management reveals a lot about a provider’s integrity. Ask: “How do you handle conflicts of interest, and do you sell proprietary products?”

The Role of Regulatory & Fiduciary Standards

Understanding who regulates your managed wealth solutions provider helps you know what protections you have.

SEC (Securities and Exchange Commission) oversight applies to investment advisors managing over $100 million in assets. These advisors must act as fiduciaries, meaning they’re legally obligated to put your interests first.

State regulators oversee smaller investment advisors. Requirements vary by state, but most require fiduciary standards similar to SEC-registered advisors.

FINRA regulation applies to broker-dealers, who operate under a “suitability” standard rather than a fiduciary standard.

For our Canadian readers, CIRO (Canadian Investment Regulatory Organization) and CIPF (Canadian Investor Protection Fund) provide similar oversight and investor protection.

More info about registered investment advisors

Costs, Technology & Risk Management Explained

Understanding the cost structure, technology capabilities, and risk management approaches of managed wealth solutions is essential for making informed decisions.

Fee Structures in Managed Wealth Solutions

Managed wealth solutions typically use fee-based compensation models, which align advisor interests with client outcomes. Here are the most common structures:

Assets Under Management (AUM) Fees: The most common model, typically ranging from 0.50% to 1.50% annually. These fees often decrease as account values increase (tiered pricing).

Flat Retainer Fees: Some advisors charge annual retainers regardless of account size. This can be beneficial for clients with complex situations but lower asset levels.

Performance Fees: Less common in traditional wealth management, these tie advisor compensation to portfolio performance above a benchmark.

Hybrid Models: Many providers combine AUM fees with project-based fees for specific services like estate planning or business succession planning.

The key is understanding what’s included. Some providers offer comprehensive planning for their standard fee, while others charge separately for financial planning services.

Technology’s Impact on Client Experience

Technology has revolutionized managed wealth solutions, making sophisticated strategies accessible to a broader range of clients. Modern platforms offer:

Robo-Hybrid Tools: Combining automated portfolio management with human oversight.

AI-Powered Rebalancing: Automated systems that continuously monitor portfolios and make adjustments based on market movements and tax considerations.

Integrated Client Portals: Providing real-time access to account information, performance reports, and financial planning documents.

Must-Have Digital Features for Modern Managed Wealth Solutions:

– Real-time account aggregation across all financial accounts

– Mobile app access with biometric security

– Document vault for important financial documents

– Goal tracking and progress monitoring

– Tax reporting and document preparation

– Secure messaging with your advisory team

– Calendar integration for scheduling meetings

The best technology doesn’t replace human advisors—it empowers them to provide better service by handling routine tasks and providing sophisticated analysis.

Integrating Banking, Lending & Insurance

Modern managed wealth solutions extend beyond investment management to include comprehensive financial services:

Cash Management: High-yield cash accounts that earn competitive rates while maintaining liquidity. Some platforms offer rates of 4.00% APY or higher on cash holdings.

Custom Credit Solutions: Including securities-based lending, mortgages, and business loans. This allows clients to access liquidity without selling investments.

Insurance Integration: Coordinating life, disability, and property insurance with overall wealth strategies.

Banking Services: Some providers offer full banking relationships, including checking accounts, credit cards, and specialized lending products.

Risk Management: Preserving Wealth Across Market Cycles

Risk management in managed wealth solutions goes far beyond diversification. It includes:

Comprehensive Risk Assessment: Understanding not just market risk, but also inflation risk, longevity risk, and sequence-of-returns risk.

Stress Testing: Analyzing how portfolios might perform under various market scenarios, including recessions, inflation spikes, and geopolitical events.

Dynamic Asset Allocation: Adjusting portfolio allocations based on changing market conditions and client circumstances.

Insurance and Protection: Using various insurance products to protect against catastrophic risks that could derail financial plans.

SIPC Protection: While not insurance, SIPC (Securities Investor Protection Corporation) provides up to $500,000 in protection if a brokerage firm fails.

More info about investor protection

Future Trends, Innovations & Real-World Success Stories

The world of managed wealth solutions is changing faster than ever. What seemed like science fiction just a few years ago is now helping real people make smarter financial decisions every day.

Emerging Innovations in Managed Wealth Solutions

Artificial intelligence is revolutionizing how we manage money. These smart systems can look at your entire financial picture and spot opportunities that human advisors might miss. They’re not replacing the personal touch—they’re making advisors even better at helping you.

ESG investing has moved way beyond just avoiding “bad” companies. Today’s managed wealth solutions can fine-tune your investments to match your personal values without sacrificing performance.

Direct indexing is a game-changer for tax-smart investing. Instead of buying an index fund, you actually own the individual stocks that make up the index. This means you can harvest tax losses on specific stocks while still getting broad market exposure.

Unified Managed Accounts are solving one of wealth management’s biggest headaches: having your money scattered across different accounts that don’t talk to each other. These platforms bring everything together.

Even cryptocurrency is finding its place in serious wealth management. The key is treating it like what it is—a speculative investment that might belong in a small corner of a well-diversified portfolio.

Case Studies: Managed Wealth Solutions in Action

Sarah and Tom needed to retire early but worried about healthcare costs. At 62, they had $2.5 million saved but faced three years without employer health insurance before Medicare kicked in. Their managed wealth solution created a tax-efficient withdrawal strategy that covered their healthcare bridge insurance while preserving their nest egg.

Mike sold his business for $15 million and faced a massive tax bill. Rather than writing a huge check to the IRS, his wealth management team structured an installment sale to spread the taxes over several years. They also set up a charitable remainder trust that satisfied his desire to give back while providing additional tax benefits.

The Johnson family wanted to pass wealth to their children without losing control. With $50 million in assets, they faced significant estate taxes. Their solution involved grantor trusts that froze the estate’s value, a family limited partnership for their business interests, and a charitable foundation that reflected their family values.

Aligning Managed Wealth Solutions with Long-Term Goals

The best managed wealth solutions don’t just focus on next quarter’s returns—they help you build the life you actually want.

Retirement security means more than just having money in the bank. It’s about creating income streams that can handle whatever life throws at you. Modern wealth solutions use sophisticated strategies to optimize Social Security, manage healthcare costs, and create withdrawal plans that adapt to changing circumstances.

Legacy building isn’t just for the ultra-wealthy anymore. Whether you want to help your kids buy their first home, support your grandchildren’s education, or leave money to causes you care about, there are smart ways to make it happen.

Philanthropic planning has become incredibly sophisticated. You can support the causes you care about while receiving significant tax benefits and even creating income streams for your family.

The thread connecting all these innovations is personalization. The future of managed wealth solutions isn’t about one-size-fits-all approaches—it’s about creating strategies as unique as the people who need them.

Frequently Asked Questions about Managed Wealth Solutions

What makes managed wealth solutions different from hiring a single financial advisor?

Think of the difference between seeing a general practitioner versus having access to an entire medical team. When you work with a single financial advisor, you’re getting one person’s expertise—which might be excellent, but has natural limitations.

Managed wealth solutions bring together multiple specialists who actually collaborate on your behalf. Your investment manager talks to your tax planner, who coordinates with your estate planning attorney, who works with your insurance specialist. This coordination is where the magic happens.

For example, let’s say you’re considering a Roth conversion. A single advisor might recommend it based on your current tax bracket. But with a team approach, your estate planner might point out how it affects your legacy planning, your investment manager might time it with a market downturn, and your tax specialist might coordinate it with other tax strategies. The result? A much more sophisticated and effective strategy.

The team approach also means you’re not vulnerable to one person’s knowledge gaps or blind spots. If your single advisor isn’t strong in estate planning or tax strategy, you might miss important opportunities. With managed wealth solutions, each specialist brings deep expertise in their area.

How much do managed wealth solutions typically cost?

Here’s the honest truth about costs: managed wealth solutions aren’t cheap, but they’re often worth every penny when you consider the complete picture.

Most providers charge between 0.75% and 1.50% of your assets annually for comprehensive wealth management. So if you have $1 million invested, you might pay $7,500 to $15,000 per year. Basic investment management alone typically costs 0.25% to 0.75%.

I know those numbers might make you wince, but here’s what we’ve seen in practice: the tax savings alone often cover the advisory fees. Add in better investment outcomes, insurance optimization, and estate planning benefits, and most clients come out significantly ahead.

Many providers use tiered fee schedules, so larger accounts pay lower percentage rates. Some offer flat retainer fees if you want comprehensive planning regardless of your asset level. The key is understanding exactly what you’re getting for your money.

This isn’t just about investment returns—it’s about optimizing your entire financial life. When done right, the value far exceeds the cost.

Can managed wealth solutions be fully automated?

This is a great question that gets to the heart of where technology fits in wealth management. The short answer is no—and you wouldn’t want them to be.

Technology excels at the routine stuff: portfolio rebalancing, tax-loss harvesting, performance reporting, and basic calculations. Modern platforms can handle these tasks more efficiently and accurately than humans ever could.

But here’s what technology can’t do: understand that you’re worried about your aging parents, help you steer a divorce, or talk you off the ledge during a market crash. It can’t coordinate complex estate planning strategies or help you balance competing financial priorities.

The most effective managed wealth solutions use what we call a “robo-hybrid” approach. Technology handles the heavy lifting on routine tasks, freeing up human advisors to focus on strategy, planning, and the relationship side of wealth management.

Think of it this way: you want your investment accounts rebalanced automatically, but you want a human being helping you decide whether to help your kids buy their first home or maximize your retirement contributions. Both are important, but they require different approaches.

At United Advisor Group, we’ve found that the best outcomes happen when technology and human expertise work together, not when one tries to replace the other.

Conclusion

Managed wealth solutions represent more than just a trend—they’re the future of how smart investors approach their financial lives. Instead of juggling multiple advisors who don’t talk to each other, you get a coordinated team working toward your specific goals.

Think about it: your investment decisions affect your taxes, your estate plan impacts your investment strategy, and your insurance needs change as your wealth grows. When these pieces work together instead of in isolation, the results can be transformative.

The wealth management industry is experiencing what many call “The Era of Independence,” where advisors are breaking free from the old broker-dealer model that prioritized selling products over serving clients. This shift has created something remarkable: truly client-first advice without the conflicts and limitations that plagued traditional wealth management.

At United Advisor Group, we’ve built our practice around this principle of independence. Our advisors have the freedom to serve clients without restrictive compliance burdens or product mandates. This means we can focus entirely on what matters most: helping you achieve your financial goals through strategies that actually make sense for your situation.

What makes managed wealth solutions so powerful is the coordination. When your investment manager understands your tax situation, when your estate planning aligns with your investment strategy, and when your insurance coverage supports your overall wealth plan, everything works better. It’s like having a symphony orchestra instead of individual musicians playing different songs.

The numbers don’t lie—we’ve seen clients save 1-2% annually in taxes through proper coordination, successfully steer major life transitions like business sales or retirement, and build legacies that reflect their values. These aren’t just investment returns; they’re life outcomes.

Your financial plan should be a “living, breathing blueprint” that grows and changes with you. Whether you’re approaching retirement, managing a business succession, planning for your family’s future, or simply wanting to make your money work smarter, the right managed wealth solution can make all the difference.

The question isn’t whether you need comprehensive wealth management—it’s whether you’re working with advisors who have the independence, expertise, and genuine commitment to put your interests first.

Ready to see how managed wealth solutions can transform your financial future? We’d love to show you what true independence looks like. More info about our services