Why Fee-Only Fiduciary Advisors Are Different

A fee only fiduciary advisor is a financial professional who receives compensation solely from client fees and is legally required to act in your best interest at all times. Here’s what makes them unique:

Key Characteristics:

- Compensation: Paid only by client fees (no commissions or kickbacks)

- Legal Standard: Bound by fiduciary duty to prioritize your interests

- Transparency: All fees disclosed upfront with no hidden costs

- Independence: No pressure to sell specific products or services

- Objectivity: Advice based purely on what’s best for your situation

Common Fee Structures:

- Hourly rates: $150-$400 per hour

- Flat fees: $1,500-$5,000 for comprehensive planning

- Asset-based: 0.75%-1.5% of assets under management annually

- Monthly retainers: $100-$400 per month

This model eliminates conflicts of interest that plague traditional advisor relationships. When your advisor isn’t earning commissions from product sales, their recommendations become truly objective.

Research shows there are only about 150 fee-only, advice-only financial planners in Canada compared to 90,000 total financial advisers – meaning less than 1% of advisors operate under this conflict-free model.

I’m Ray Gettins, and through my work with United Advisor Group, I’ve seen how exceptional advisors thrive when they can operate as a fee only fiduciary advisor without the constraints of proprietary products or commission pressures.

What Is a Fee-Only Fiduciary Advisor?

A fee only fiduciary advisor combines two critical elements that protect your financial interests:

Fee-Only Structure: The advisor receives 100% of their compensation directly from you. They don’t earn commissions from selling insurance products, mutual funds, or other financial instruments. No kickbacks, no referral fees, no hidden revenue streams.

Fiduciary Duty: This is a legal obligation requiring the advisor to act in your best interest at all times. They must:

- Put your interests above their own

- Disclose any potential conflicts of interest

- Provide advice based on what’s genuinely best for your situation

- Maintain transparency about their compensation and recommendations

Most fee only fiduciary advisors operate as Registered Investment Advisors (RIAs) under SEC or state regulation. Many also hold the Certified Financial Planner (CFP) designation, which requires additional education and adherence to strict ethical standards.

Core Features of a Fee Only Fiduciary Advisor

Legal Obligation: Unlike advisors who operate under suitability standards, fiduciaries are legally bound to prioritize your interests.

Complete Objectivity: When an advisor’s income doesn’t depend on selling you specific products, their recommendations become purely objective.

Full Disclosure: Every potential conflict of interest must be disclosed in writing.

Comprehensive Planning: Since they’re not focused on product sales, fee only fiduciary advisors typically provide more holistic financial planning.

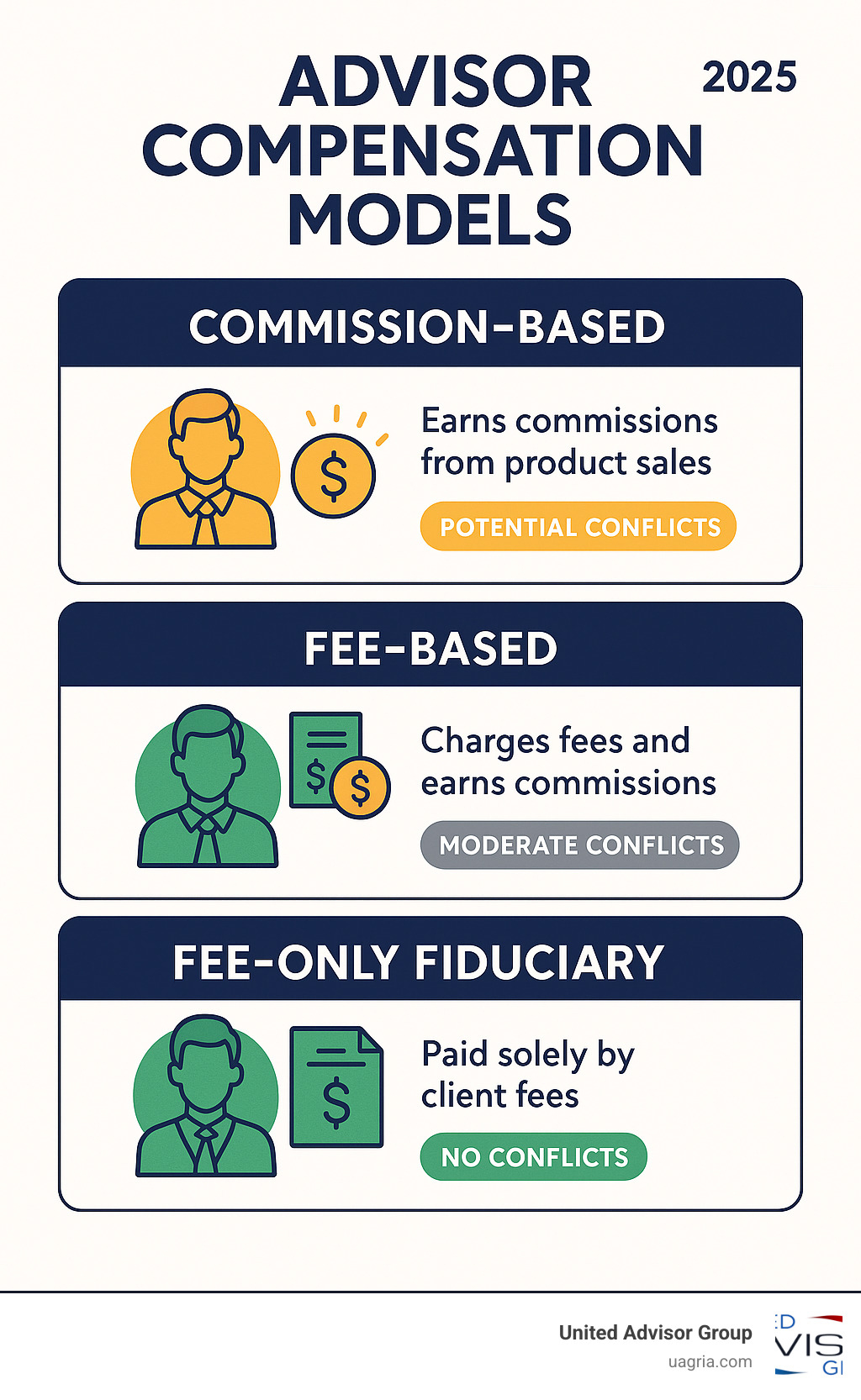

How the Term “Fee Only Fiduciary Advisor” Differs From Fee-Based & Commission Models

Commission-Based Advisors earn money when you buy or sell financial products. This creates an inherent conflict – they make more money when you transact more frequently or purchase higher-commission products.

Fee-Based Advisors use a hybrid model combining fees and commissions. They might charge you a planning fee and also earn commissions on products they sell.

Fee Only Fiduciary Advisors eliminate these conflicts entirely. As one industry expert noted, “Fee-only, advice-only financial planners are compensated solely by agreed-upon fees paid by the client. This means there are no hidden costs, third party financial motivations or kick-backs.”

Independent Financial Advice becomes truly independent when these structural conflicts are removed.

Fee Structures & Real-World Costs

Understanding how fee only fiduciary advisors charge helps you make smart decisions and avoid surprises. The beauty is transparency – you’ll know exactly what you’re paying and why.

| Fee Structure | Typical Range | Best For | Pros | Cons |

|---|---|---|---|---|

| Hourly | $150-$400/hour | Specific questions, one-time advice | Pay only for time used, flexible | Can be unpredictable |

| Flat Fee | $1,500-$5,000 | Comprehensive financial plans | Predictable cost | May not fit complex situations |

| AUM-Based | 0.75%-1.5% annually | Ongoing investment management | Aligns advisor success with yours | Costs increase with assets |

| Monthly Retainer | $100-$400/month | Ongoing planning relationship | Predictable, encourages communication | Ongoing commitment required |

With $500,000 saved for retirement, you might pay:

$3,000 for hourly planning – About 10 hours at $300 per hour for comprehensive planning.

$3,500 for a flat-fee plan – One comprehensive financial plan covering retirement projections to tax strategies.

$5,000 annually for ongoing management – That’s 1% of your $500,000 portfolio for investment management and ongoing guidance.

$2,400 per year for monthly retainer – Just $200 monthly for regular check-ins and ongoing support.

Research consistently shows that working with a qualified advisor can add 1.5% to 3% annually to your returns through smarter tax planning, avoiding costly mistakes, and staying disciplined during market turbulence.

On that $500,000 portfolio, an extra 2% annually equals $10,000 in additional value. Even after paying advisor fees, you come out ahead. Plus, investment advisory fees are often tax-deductible.

The key difference with fee-only advisors is what you don’t pay. No hidden mutual fund kickbacks. No commission charges when you buy or sell. No pressure to choose expensive products because they pay the advisor more.

Registered Investment Advisor: Enhancing Client Relationships explores how this transparent approach builds trust.

Common Pricing Options for a Fee Only Fiduciary Advisor

Hourly billing works when you have specific questions or need occasional guidance. Newer advisors often charge closer to $150 per hour, while experienced professionals in major cities might charge $400 or more.

Flat fees give you comfort knowing your total cost upfront. Most comprehensive financial plans fall between $1,500 and $5,000, covering everything from analyzing your current situation to creating detailed recommendations.

Asset-based fees align your advisor’s success with yours – they do better when your portfolio grows. However, 1% annually on $1 million equals $10,000 per year.

Monthly retainers are gaining popularity, especially among younger professionals. For $100 to $400 monthly, you get ongoing access without large upfront costs or asset minimums.

Many fee only fiduciary advisors blend these approaches, charging a flat fee for initial planning, then switching to a monthly retainer for ongoing support.

Benefits and Potential Drawbacks

The biggest advantage? Your advisor’s success depends entirely on your satisfaction. They’re not trying to hit sales quotas or push products that pay higher commissions.

This alignment of interests creates truly holistic planning. Your advisor might tell you to pay off credit cards before investing more, suggest you need less life insurance, or even recommend working with a different advisor if your needs don’t match their expertise.

Unbiased product selection means your advisor can choose from the entire universe of investment options, often translating to lower costs and better performance – sometimes saving thousands annually in hidden fees.

You’ll also experience complete transparency about costs. No surprises, no hidden fees, no wondering if recommendations serve your interests or your advisor’s wallet.

But let’s talk about potential downsides:

Higher upfront costs can be jarring if you’re used to “free” advice from commission-based advisors. That comprehensive financial plan might cost $3,000 upfront instead of being “included” with product purchases.

Some fee only fiduciary advisors have limited product access because they don’t sell insurance or handle certain transactions, potentially requiring additional professionals for comprehensive services.

State restrictions can limit what your advisor can do. In some areas, regulations prevent fee-only advisors from providing certain insurance guidance.

For people with smaller account balances, the economics can be challenging. If you have $50,000 to invest, paying $2,500 for financial planning represents 5% of your assets.

Research consistently shows that benefits typically outweigh these drawbacks. As scientific research on conflict-free advice demonstrates, fee only fiduciary advisors often charge higher upfront costs, but this gets offset by receiving unbiased advice and avoiding hidden charges over time.

Why Transparency Matters

The psychological comfort of knowing your advisor has no hidden agenda often leads to better financial decisions on your part.

Objectivity in advice creates genuine trust. When you know your advisor isn’t earning more money by recommending frequent trading or expensive products, you can focus on the actual strategy.

Your advisor can focus on long-term outcomes instead of quarterly sales targets. They might recommend a simple, boring investment strategy that works beautifully over decades.

The psychological comfort of transparency extends beyond knowing the costs. During the 2008 financial crisis, fee-only advisors could provide unbiased behavioral coaching, helping clients stay invested when emotions screamed “sell everything.”

Advisor Autonomy Benefits explores how this independence creates better outcomes for everyone involved.

How to Verify and Choose the Right Fee-Only Fiduciary Advisor

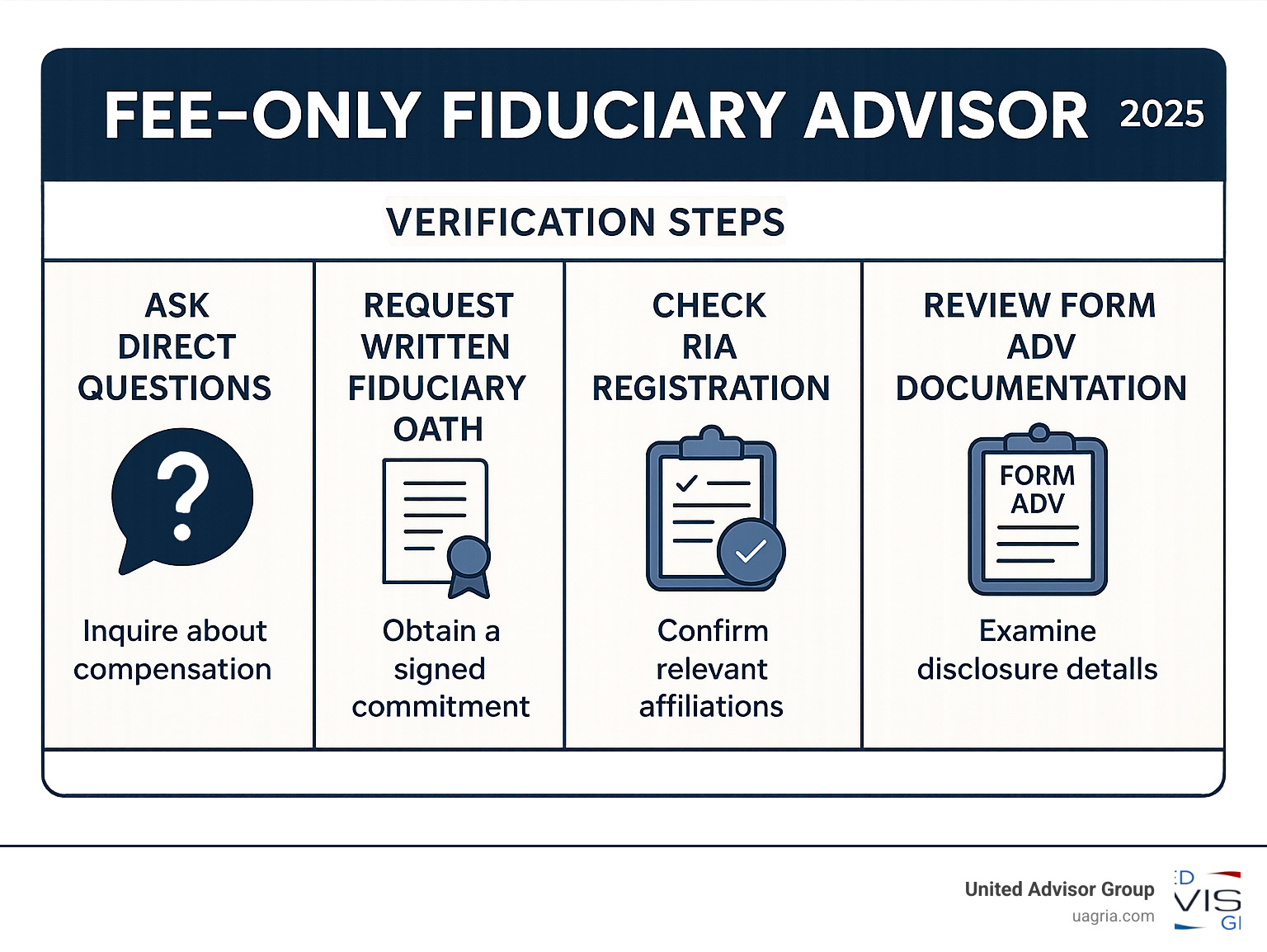

Finding a genuine fee only fiduciary advisor isn’t about taking someone’s word for it. It’s about doing your homework and asking the right questions.

Start with the paper trail. Every legitimate fee-only advisor must be registered as a Registered Investment Advisor (RIA) with either the SEC or their state. You can verify their registration through the SEC’s Investment Adviser Public Disclosure database. Check out their Form ADV, which shows their fees, business practices, and any past disciplinary issues.

Ask for written proof. A real fee only fiduciary advisor won’t hesitate to put their commitments in writing. They should provide you with a written fiduciary oath, a detailed fee schedule, and their Form ADV Part 2.

Professional associations make your search easier. NAPFA members must be fee-only and sign a fiduciary oath. The XY Planning Network focuses on fee-only advisors who work with younger professionals, while the Garrett Planning Network specializes in hourly planning.

Credentials matter. Look for designations like CFP (Certified Financial Planner), which requires extensive education and adherence to fiduciary standards. CFA (Chartered Financial Analyst) shows deep investment knowledge, while PFS (Personal Financial Specialist) is for CPAs who specialize in financial planning.

Don’t skip the background check. Search FINRA BrokerCheck if they hold securities licenses, check state insurance departments if they sell insurance, and Google them. A clean record doesn’t guarantee future performance, but a messy past often predicts future problems.

The Financial Advisor Comparison Tool gives you a systematic way to evaluate and compare different advisors.

Must-Ask Questions for a Prospective Fee Only Fiduciary Advisor

The money questions come first. Ask directly: “Are you fee-only and fiduciary 100% of the time?” Follow up with “Do you receive any commissions, referral fees, or other compensation from third parties?” A true fee-only advisor will explain their compensation structure clearly.

Get specific about costs. “What is your exact fee structure, and are there any additional costs I should expect?” should get you a detailed breakdown.

Understand their approach. Ask “What specific services do you provide, and what do you refer out to other professionals?” Good advisors know their strengths and have trusted partners for areas outside their expertise.

Know their client base. “Who is your typical client, and do you have minimums?” helps you understand if you’re a good fit.

Plan for the future. “What happens to my relationship if you retire or leave the business?” shows the advisor thinks long-term about client relationships.

A legitimate fee only fiduciary advisor will welcome tough questions and answer them directly. If someone gets defensive or tries to change the subject, that tells you something important.

Key Considerations for Selecting a Financial Advisor in D.C. dives deeper into the selection process, though these principles work anywhere.

Client–Advisor Relationship: What to Expect

Starting a relationship with a fee only fiduciary advisor feels refreshingly different. There’s no sales pitch, no pressure to buy products, and no hidden agenda – just genuine focus on your financial success.

Your journey typically begins with a no-obligation conversation. You’ll discuss your goals, current financial situation, and get a feel for whether you click with the advisor. If you both decide to move forward, you’ll receive a clear engagement letter spelling out exactly what services you’ll receive and how much you’ll pay.

The Findy Phase

Your advisor becomes part financial detective, part trusted confidant. They’ll want to understand your complete financial picture – your current assets and debts, income and spending patterns, and those financial goals you’ve been thinking about. They’ll also explore your risk tolerance and family dynamics that impact your financial strategy.

Creating Your Roadmap

Based on what they learn, your advisor will craft a comprehensive financial plan personalized for your situation. This includes cash flow optimization strategies, clear investment allocation designed to match your goals, and retirement projections showing whether you’re on track.

Tax planning becomes an ongoing conversation rather than an annual scramble. Your advisor will identify opportunities for tax-efficient strategies throughout the year and coordinate with your other professionals.

The Ongoing Partnership

Implementation is where real value shows up. Fee only fiduciary advisors typically help you put their recommendations into action, assisting with setting up accounts and coordinating automatic transfers.

Regular check-ins become the heartbeat of your relationship. Whether quarterly phone calls or annual meetings, these sessions keep you accountable and your plan current. Your advisor will monitor your progress, suggest adjustments when life changes, and provide crucial behavioral coaching when markets get scary.

Many advisors now offer virtual meetings and online portals that make staying connected convenient. The collaborative nature often surprises people – conversations feel more honest and educational because there’s no sales agenda.

Understanding Independent Fiduciary & Virtual Family Office Roles explores how this collaborative approach extends to complex family situations.

Service Menu Typically Provided

Investment policy development starts with creating your personal Investment Policy Statement. Your advisor will design a portfolio aligned with your goals and provide ongoing management, including regular rebalancing and tax-loss harvesting.

Retirement planning goes beyond simple calculations. Using sophisticated software, your advisor will model different scenarios, helping you understand not just how much to save, but when you might retire and how to structure withdrawals.

Tax planning becomes a year-round strategy. Your advisor will identify opportunities for Roth conversions, coordinate tax-loss harvesting, and explore charitable giving strategies.

Insurance analysis focuses purely on your protection needs since your advisor doesn’t earn commissions from insurance sales.

Estate planning coordination ensures your financial plan works harmoniously with your legal documents.

Cash flow coaching and budgeting support helps you optimize your spending and saving patterns.

Perhaps most importantly, your advisor provides accountability and behavioral coaching, helping you stay disciplined during market volatility and maintain focus on long-term objectives.

Frequently Asked Questions about Fee-Only Fiduciary Advisors

Are all fee-only advisors automatically fiduciaries?

While most fee-only advisors are fiduciaries, it’s not automatic. Fee-only describes how they get paid, while fiduciary describes their legal obligation to you.

To verify you’re getting both, ask: “Do you receive ANY compensation from third parties – commissions, referral fees, or kickbacks?” A true fee only fiduciary advisor will answer with a clear “no” and provide written documentation.

Most legitimate advisors will provide a written fiduciary oath without hesitation. Also check that they’re registered as a Registered Investment Advisor (RIA), which typically requires fiduciary adherence.

Organizations like NAPFA make this easier by requiring both fee-only compensation AND fiduciary commitment from all members.

Will I pay more overall compared to a commission advisor?

You’ll likely pay more upfront but save significantly over time.

The upfront reality: Yes, you’ll typically pay more initially. A fee only fiduciary advisor can’t subsidize their planning costs with ongoing product commissions, so that comprehensive financial plan might cost $2,000 to $5,000 right away.

But commission-based advisors might not charge you directly for planning, but you’ll pay through higher ongoing costs that compound over decades. High-commission products can cost 1% to 3% more annually than the low-cost alternatives a fee-only advisor would recommend.

If you have a $500,000 portfolio, that extra 1% to 3% in annual costs equals $5,000 to $15,000 every single year. Over 20 years, those “hidden” costs could easily exceed $200,000 – far more than you’d ever pay a fee only fiduciary advisor.

How do I confirm an advisor is truly fee-only and fiduciary?

Start with direct questions: “Are you fee-only and fiduciary 100% of the time?” followed by “Do you receive ANY compensation from third parties?” A legitimate advisor will give you clear, straightforward answers.

Ask for written proof. Request their Form ADV Part 2, a written fiduciary oath, and a detailed fee agreement. If they hesitate, that’s a red flag.

Verify their registration through the SEC’s Investment Adviser Public Disclosure database or your state securities regulator.

Check their professional memberships. NAPFA membership requires both fee-only compensation and fiduciary commitment. The CFP designation also requires adherence to fiduciary standards.

Watch for red flags: Vague answers about how they’re paid, reluctance to provide documentation, mentions of “preferred” products, or inability to clearly explain their fee structure.

A true fee only fiduciary advisor will welcome these questions enthusiastically. This verification process protects your financial future.

Conclusion

Choosing a fee only fiduciary advisor isn’t just about finding someone to manage your money – it’s about partnering with someone who’s legally bound to put your interests first, every single time.

When your advisor’s success depends entirely on your success rather than on selling you products, everything changes. The advice becomes genuinely objective. The recommendations focus on what’s truly best for your situation. The relationship transforms into a collaborative partnership aimed at maximizing your financial well-being.

The numbers tell the story. With less than 1% of financial advisors operating under the true fee-only fiduciary model, you’re accessing something genuinely rare – complete transparency and zero conflicts of interest.

Yes, you might pay more upfront. But you get better investment returns through lower-cost products, superior tax planning that can save thousands annually, unbiased recommendations that serve your needs, and genuine accountability during both good times and market turbulence.

Finding the right advisor takes effort. Use those verification steps we outlined. Ask the tough questions about compensation. A legitimate fee only fiduciary advisor will welcome your scrutiny and provide complete transparency.

This becomes more than a professional relationship – it evolves into a lifelong partnership focused on your financial success. When your advisor only wins when you win, you’ve found the alignment that leads to optimal outcomes.

Through my work with United Advisor Group, I’ve seen this change countless times. We’ve deliberately structured our organization to free advisors from proprietary product pressures and commission conflicts. This independence allows our advisors to provide the objective, client-first advice that makes a real difference in people’s financial lives.

Your financial future deserves this level of commitment. It deserves an advisor who’s legally obligated to act in your best interest, who earns money only when they provide value to you, and who can recommend any solution based purely on what serves your goals.

More info about independent services – United Advisor Group empowers you to work with a fee only fiduciary advisor who puts your interests first, always.

The choice is straightforward: continue with traditional advisory models where conflicts of interest are built into the compensation structure, or step into fee-only fiduciary advice where your success becomes the only measure of your advisor’s success.