Why Asset Allocation for Retirement Is Your Financial Foundation

What Are You Working With? The Building Blocks of Your Portfolio

Think of your investment portfolio like a delicious, well-balanced meal. You wouldn’t just eat dessert, right? (Well, maybe sometimes, but not for long-term health!). Similarly, a healthy asset allocation for retirement needs a mix of different ingredients, or “asset classes,” each playing a unique role in your overall portfolio construction.

Stocks (The Growth Engine)

Stocks represent tiny pieces of ownership in companies. They’re like the powerful engine of your portfolio, offering the biggest potential for your money to grow over the long run. But just like a powerful engine, they can also have a bumpy ride sometimes, meaning more market volatility. Historically, though, stocks have been your best friend for outpacing inflation and building wealth over many decades.

Within stocks, you can spread your money even further:

- U.S. Large-Cap: These are the giant, well-known companies you see everywhere, like those in the S&P 500. Think of them as the steady, reliable leaders. The New York State Common Retirement Fund, for example, puts a big chunk (60%) of its U.S. stock money into these, showing how important they are.

- U.S. Small-Cap: These are smaller, younger companies. They might not be household names yet, but they have the potential for faster growth. Of course, with that higher potential comes a bit more risk.

- International Equities (Developed & Emerging Markets): Investing outside the U.S. is like exploring new flavors! It helps your portfolio stay strong by not putting all your eggs in one basket. Developed international markets are like the established, stable economies (think Europe or Japan), while emerging markets are countries that are growing rapidly (like parts of Asia or South America). They offer exciting growth but can be more volatile.

The big takeaway? Even in retirement, stocks are super important for growth. They help make sure your money lasts as long as you do, especially since we’re all living longer and longer!

Bonds (The Stabilizer)

If stocks are the thrilling roller coaster, bonds are the steady, comfortable train ride. When you buy a bond, you’re essentially lending money to a government or a company. In return, they promise to pay you interest regularly. Bonds play a crucial role in your asset allocation for retirement because they provide a steady income, help calm down your portfolio when markets get choppy, and work to protect your original money.

Here are some common types of bonds:

- U.S. Treasury Bonds: These are loans to the U.S. government. Because they’re backed by the government, they’re considered very, very safe.

- Corporate Bonds: These are loans to companies. They usually offer higher interest rates than Treasuries because there’s a bit more risk involved.

- Nontraditional Bonds & High Yield Bonds: These are for investors willing to take on more risk for potentially higher returns. Big institutions often use a portion of these in their bond mix.

- International Bonds: Just like with stocks, investing in bonds from other countries can add more diversity to your portfolio.

- Inflation-Protected Securities (TIPS): These are special government bonds designed to protect your money from rising prices. Their value adjusts with the Consumer Price Index, helping you keep up with inflation.

While bonds generally don’t grow as fast as stocks, their stability can be a real lifesaver during tough market times. For instance, during the stock market downturn from 2000-2002, a portfolio with 80% bonds and just 20% stocks actually saw positive returns after inflation. Meanwhile, a portfolio that was 80% stocks and 20% bonds lost a lot of value. That’s the power of bonds!

Cash & Equivalents (The Safety Net)

Cash is king when you need quick access to your money and want to feel secure. These are assets you can get your hands on fast, without worrying about market ups and downs.

Your cash portion serves a few key purposes:

- Emergency Fund: Experts recommend keeping enough cash to cover 6 to 12 months of your living expenses. This way, if something unexpected happens, you’re not forced to sell your investments at a bad time.

- Planned Expenses: For retirees, cash acts as a handy buffer. It covers your immediate spending needs so you don’t have to touch your more volatile investments when the market is down. This helps avoid something called “sequence of returns risk,” which we’ll talk more about later!

- Opportunity: Sometimes, having cash ready allows you to jump on great investment opportunities when the market takes a dip.

Options for your cash and its close relatives include:

- High-Yield Savings Accounts: These offer competitive interest rates and let you access your money anytime.

- Money Market Funds: Similar to savings accounts, but sometimes with slightly better interest rates.

- Certificates of Deposit (CDs): With a CD, you agree to keep your money locked up for a set period, and in return, you get a fixed interest rate. In July 2023, some CDs were offering yields around 5.3%, which made them quite appealing for short-term savings! You can even create a “CD ladder” by buying CDs that mature at different times, giving you regular access to funds.

Just remember, while cash offers safety, it usually doesn’t grow fast enough to beat inflation over the long term. So, it’s best kept for your immediate needs and as a protective layer, not for long-term growth.

Alternatives (The Diversifiers)

Beyond the usual suspects – stocks, bonds, and cash – some investors, especially large funds like the New York State Common Retirement Fund, also include “alternative” assets in their portfolios. These are designed to add even more variety and potentially boost returns or reduce risk in different market conditions.

Some examples from these big funds include:

- Private Equity (15%): This is money invested directly into companies that aren’t traded on public stock exchanges.

- Real Estate (12%): Owning properties, either directly or through special funds.

- Real Assets (4%): These are tangible things like infrastructure (roads, bridges), timberland (forests), or commodities (like gold or oil).

- Credit (4%): Various forms of lending, often with higher yields than typical bonds.

- Opportunistic/Absolute Return Strategies (3%): These are flexible strategies that aim to make money no matter what the market is doing.

For individual investors like you and me, direct access to some of these might be tricky. However, you can often get exposure to things like real estate through REITs (Real Estate Investment Trusts) or commodities through certain funds. The key is that these alternatives behave differently from stocks and bonds, adding another important layer of diversification to your asset allocation for retirement.

Finding Your Perfect Mix: A Personalized Asset Allocation for Retirement

Now that we’ve met the players – stocks, bonds, and cash – how do you decide how much of each should be on your team? This is where your asset allocation for retirement becomes deeply personal. There’s no magic, one-size-fits-all answer here. Your ideal mix depends on factors unique to you: your age, how comfortable you are with ups and downs (your risk tolerance), how long you have until you need the money (your time horizon), and even how long you expect to live (longevity risk!).

At United Advisor Group, we believe in crafting Custom Investment Solutions that align perfectly with your individual circumstances. It’s like tailoring a suit – it just fits better when it’s made for you.

Start with Simple Rules of Thumb

While we’ll dive into personalization, some general guidelines can give you a helpful starting point. Think of them as a basic recipe before you add your personal flair and special spices:

First, there’s John Bogle’s ‘Age in Bonds’ Rule. This classic idea suggests that the percentage of your portfolio in bonds should roughly equal your age. So, if you’re 60, you’d aim for 60% bonds and 40% stocks. This makes sense because as we get older, we usually have more wealth to protect and less time to recover if the market takes a big dip.

Then, there’s the slightly more adventurous ‘110 or 120 Minus Age’ Rule. This one suggests you subtract your age from 110 or 120 to figure out your stock allocation. For a 60-year-old, that could mean 50-60% in stocks (110-60=50, 120-60=60). This rule acknowledges that people are living longer, healthier lives, and might need a bit more growth to make their money last.

Finally, Benjamin Graham’s 25-75% Stock Rule from the “father of value investing” suggests never having less than 25% or more than 75% of your money in stocks. The rest would be in bonds. This implies that a 50-50 split is a perfectly balanced starting point.

These rules are simple and easy to remember, but remember, they are just guides. Your personal situation might call for some thoughtful adjustments.

Assess Your Personal Risk Profile

This is where the real digging begins. Your personal risk profile isn’t just about how much risk you want to take. It’s also about how much risk you can afford to take, and sometimes, how much risk you need to take to reach your goals.

There’s a really important difference between:

- Risk Tolerance: This is your gut feeling, your emotional comfort level with market ups and downs. If the market dropped 20% tomorrow, would you be able to sleep at night, or would you be pacing the floor? As Kiplinger’s aptly puts it, “Risk tolerance is based on emotion and measures how much you will panic when the market drops.”

- Risk Capacity: This is the more mathematical side. It’s your actual ability to handle losses without derailing your financial future. For example, if you have a rock-solid pension covering all your essential expenses, your capacity to take on investment risk might be much higher than someone relying solely on their investment portfolio.

We often use special tools and have detailed conversations to help you figure out both of these important aspects. For a deeper dive into understanding your risk tolerance, you might find articles like Asset Allocation Guide: What is your risk tolerance? helpful.

Your financial goals (what you’re saving for), your retirement timeline (when you actually need to start drawing from your savings), and any other income sources you might have (like Social Security or a pension) all play a big role. If you’re fortunate enough to have a guaranteed pension that covers most of your everyday bills, you might be able to keep a bit more of your money in growth-oriented investments, even into your later retirement years.

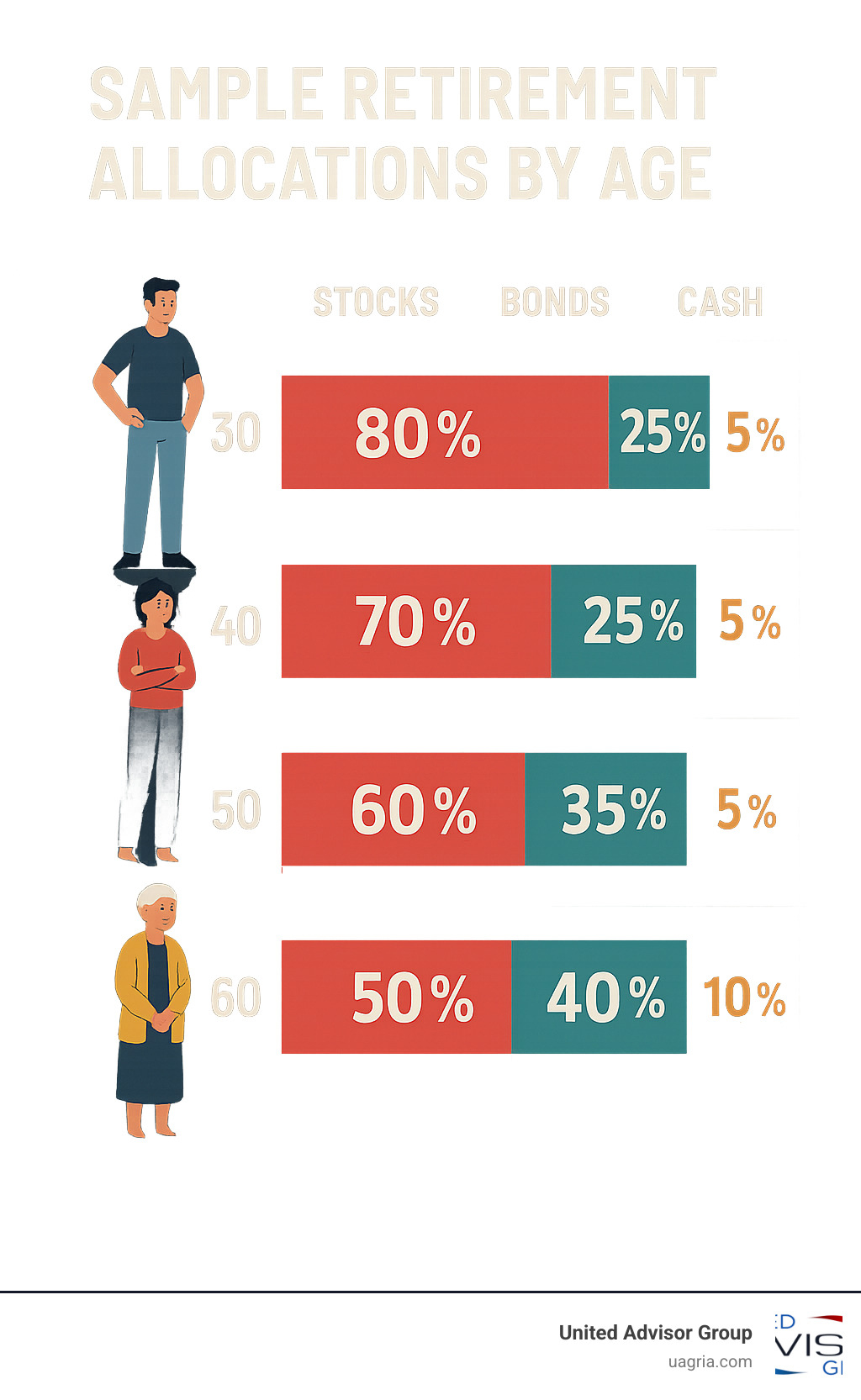

Sample asset allocation for retirement by Age

While we can’t stress enough that personalization is key, here are some commonly suggested portfolio allocations for retirees. These general guidelines aim to balance the need for growth with the desire for preservation as you move through your golden years. They illustrate the typical shift towards more conservative investments over time:

| Age Range | Stock Allocation | Bond Allocation | Cash/Cash Investments |

|---|---|---|---|

| 60-69 | 60% | 35% | 5% |

| 70-79 | 40% | 50% | 10% |

| 80 and above | 20% | 50% | 30% |

Please remember, these figures are just a general guide. Your specific asset allocation for retirement might look quite different based on your unique risk profile, the retirement lifestyle you dream of, and any other financial resources you have. That’s why having a trusted advisor by your side can make all the difference.

Protecting Your Nest Egg: Strategies for a Volatile World

Building a retirement portfolio is a huge milestone\u00197but the real challenge is keeping it intact when markets get rough. Smart asset allocation for retirement is your first line of defense, especially against two big threats:

- Sequence-of-returns risk: Large market drops early in retirement can shorten the life of your nest egg because you\u0019re selling investments at low prices while also drawing income.

- Inflation: Even mild inflation chips away at your purchasing power over a long retirement.

The “Bucket” Strategy

A simple way to lower these risks is to divide your money into three time-based “buckets.”

Bucket 1\u0019Safety Net (1\u00096 years)

Cash, money-market funds, or very short-term CDs cover day-to-day spending. Because this bucket isn\u0019t tied to the market, you avoid selling stocks in a downturn.Bucket 2\u0019Income (5\u000910 years)

Intermediate-term bonds and dividend-paying stocks provide income and a modest growth cushion. As Bucket 1 is used, you periodically refill it from here.Bucket 3\u0019Growth (10 + years)

Long-term growth assets\u0019primarily diversified stock funds and, if appropriate, select alternatives\u0019live here. They combat inflation and replenish the first two buckets after markets recover.

The structure may look different for every retiree, but the goal is the same: give short-term spending needs a safe home while giving long-term dollars time to rebound.

Battling Inflation and Recession

History shows that a diversified mix of stocks has been the most reliable way to outpace inflation, while bonds and cash provide stability when growth assets stumble. From the 1960s through 2023, broad U.S. stock indexes recovered from bear markets in roughly 3\u00189\u00189 years on average. Having cash in Bucket 1 means you can wait out those recoveries.

Coordinate All Income Sources

Don\u0019t view your portfolio in isolation. Guaranteed income\u0019Social Security, pensions, and lifetime annuities\u0019resembles a bond-like stream you can count on to pay the basics. Variable income\u0019withdrawals from your investments\u0019can cover the more flexible parts of your budget. Factoring these together often lets retirees maintain a bit more growth in Bucket 3 without losing sleep.

Need help designing buckets or deciding how much guaranteed income you really need? Our team can incorporate these pieces into a broader Retirement and Tax Planning strategy so your money works efficiently no matter what the market does.

Keeping Your Plan on Track: The Importance of Review and Rebalancing

Your asset allocation for retirement isn’t a “set it and forget it” kind of deal. Think of it more like tending a vibrant garden. You plant the seeds (your initial allocation), but then you need to prune, water, and fertilize to keep it healthy and growing strong.

Over time, markets fluctuate, and your life changes. What happens is that your portfolio’s actual allocation will naturally “drift” away from your original target. Maybe your stocks have had a fantastic run, making them a much larger part of your portfolio than you intended. Or perhaps bonds have dipped, leaving you with a smaller percentage than planned. This drift can quietly shift your risk level without you even realizing it.

That’s why regular review and rebalancing are so essential. It’s how you maintain your desired risk level and ensure your portfolio continues to align with your financial goals. We believe in Collaborative Financial Planning to ensure your plan stays on track, adapting as life unfolds. An annual review is a great habit, but major life events – like a new grandchild, a health change, or an unexpected inheritance – are also prime times to take a fresh look. Remember to consider any tax implications when selling assets, especially in taxable accounts.

Why, How, and When to Rebalance Your Portfolio

So, why bother rebalancing? The main reason is to maintain your target allocation and, by extension, your comfort level with risk. If stocks have soared, your portfolio might now be riskier than you planned. If they’ve dropped, your bond portion might be too large, potentially limiting your long-term growth. Rebalancing brings your portfolio back to your chosen percentages, keeping you on the path you set. It’s also a disciplined, smart way to “sell high and buy low” without trying to guess market movements.

As for how to rebalance, it’s quite straightforward. You simply sell some of the asset classes that have performed well (and now make up a larger percentage of your portfolio) and use that money to buy more of the asset classes that have lagged behind (and now represent a smaller portion). This gently nudges your portfolio back to its intended mix.

Finally, when to rebalance? You have a couple of good options:

- Calendar-Based: Many people choose to rebalance annually, perhaps at the start of a new year, or semi-annually. This is a simple, consistent approach that ensures you check in regularly.

- Percentage-Based (Threshold): This method is a bit more active. You decide on a certain percentage deviation from your target. For example, if your target stock allocation is 60%, you might decide to rebalance only if it climbs above 65% or drops below 55%. This means you only act when necessary, saving you time if the market is relatively stable.

No matter which method you choose, understanding asset allocation for retirement and the role of rebalancing is key to keeping your financial future secure.

Frequently Asked Questions about Retirement Asset Allocation

You’ve got questions about how to best manage your money in retirement, and that’s fantastic! It shows you’re thinking proactively about your financial future. Let’s tackle some common queries about asset allocation for retirement.

How much cash should I hold in retirement?

This is a great question, and one many retirees ponder! Think of your cash as your immediate “comfort fund.” A widely accepted guideline is to keep 6 to 12 months of your estimated living expenses readily available in highly liquid accounts, like a high-yield savings account. This acts as your personal emergency fund, ensuring you can cover unexpected costs without touching your investments.

Beyond that initial safety net, many savvy retirees use a strategy we touched on earlier: the “bucket” strategy. This involves setting aside an additional 1 to 2 years of planned spending in cash or cash equivalents. Why? Because it gives you a buffer. If the stock market takes a tumble, you won’t be forced to sell your growth investments at a loss to pay your bills. You can simply draw from your cash bucket, allowing your other assets time to recover. It’s like having a deep pantry for your financial needs!

What is a “glide path”?

Imagine you’re flying a plane towards retirement. A “glide path” is essentially your planned descent. In investing terms, it’s the gradual, pre-planned shift in your portfolio’s asset allocation over time. As you get closer to, and then move through, retirement, your portfolio slowly “glides” from being more aggressive (meaning a higher percentage in stocks) to more conservative (a higher percentage in bonds and cash).

The idea behind a glide path is simple: you generally need more growth when you’re younger to build your nest egg, and more stability as you age to protect it. Some investment solutions, especially target-date funds, are actually designed to follow a specific glide path automatically, making the process smoother for you. It’s a systematic way to adapt your asset allocation for retirement as your needs and time horizon change.

Can I be too conservative with my retirement asset allocation?

Oh, absolutely! While protecting your hard-earned savings is incredibly important, being too conservative, especially early in a potentially long retirement, can surprisingly become a significant risk itself.

Think about it: retirement isn’t just a few years anymore. Many of us are looking at 25 to 30+ years of golden years! If your money isn’t growing at all, you face two big challenges:

- Inflation Risk: This is where the purchasing power of your money slowly but surely decreases over time. What $100 buys today might only buy $70 in 10 or 15 years. If your money is just sitting there, it’s losing value to rising prices.

- Longevity Risk: This is the scary thought of outliving your savings. If your money isn’t growing, and you’re living longer than expected, you could find your funds depleted sooner than planned.

Even in retirement, a small, thoughtful allocation to growth assets like stocks is often crucial. It helps your money keep pace with inflation and ensures your purchasing power lasts for your entire retirement journey. It’s all about finding that sweet spot in your asset allocation for retirement – enough growth to last, and enough stability to sleep well at night!

Conclusion

Navigating asset allocation for retirement might sound like a complex financial puzzle, but it doesn’t have to be overwhelming. At its heart, it’s about understanding the basic “ingredients” in your financial pantry, mixing them in a way that feels right for you, and then keeping a watchful eye on that mix over time.

So, what’s the big picture here? We’ve learned that your asset allocation for retirement isn’t just a decision; it’s the decision, influencing a whopping 88% of your investment journey. It’s like building a balanced meal: you need stocks for growth (your energetic main course!), bonds for stability (the comforting side dish), and cash for that cozy safety net (your emergency snack stash).

And because your life is unique, your allocation should be too. It’s all about personalizing it to your age, your comfort with risk, how long you have, and even your other income sources like Social Security or a pension. We also talked about how to protect your hard-earned savings using smart strategies like the “bucket” approach to help you brave those market storms and fight off inflation.

Finally, remember your portfolio isn’t a static painting; it needs regular review and rebalancing to stay aligned with your evolving life and the ever-changing market. This helps keep your plan on track, ensuring it continues to support your dreams.

At United Advisor Group, we’re passionate about empowering our clients with custom financial solutions. We truly believe in client-focused service, free from the pressures of selling specific products. This approach means your financial plan is truly built around your needs, giving you genuine financial independence.

You certainly don’t need to be a math whiz to have a successful retirement. You just need a clear understanding of these core principles and a commitment to your own long-term financial well-being. If you’re ready to create a personalized asset allocation for retirement that helps you sleep soundly and confidently pursue your financial dreams, we’re here to help guide you.