The Critical Role of a Retirement Tax Planning Advisor

Finding the right retirement tax planning advisor near me can make the difference between a comfortable retirement and running out of money. If you’re searching for local expertise, here’s what you need to know immediately:

Quick Answer for Finding a Retirement Tax Planning Advisor:

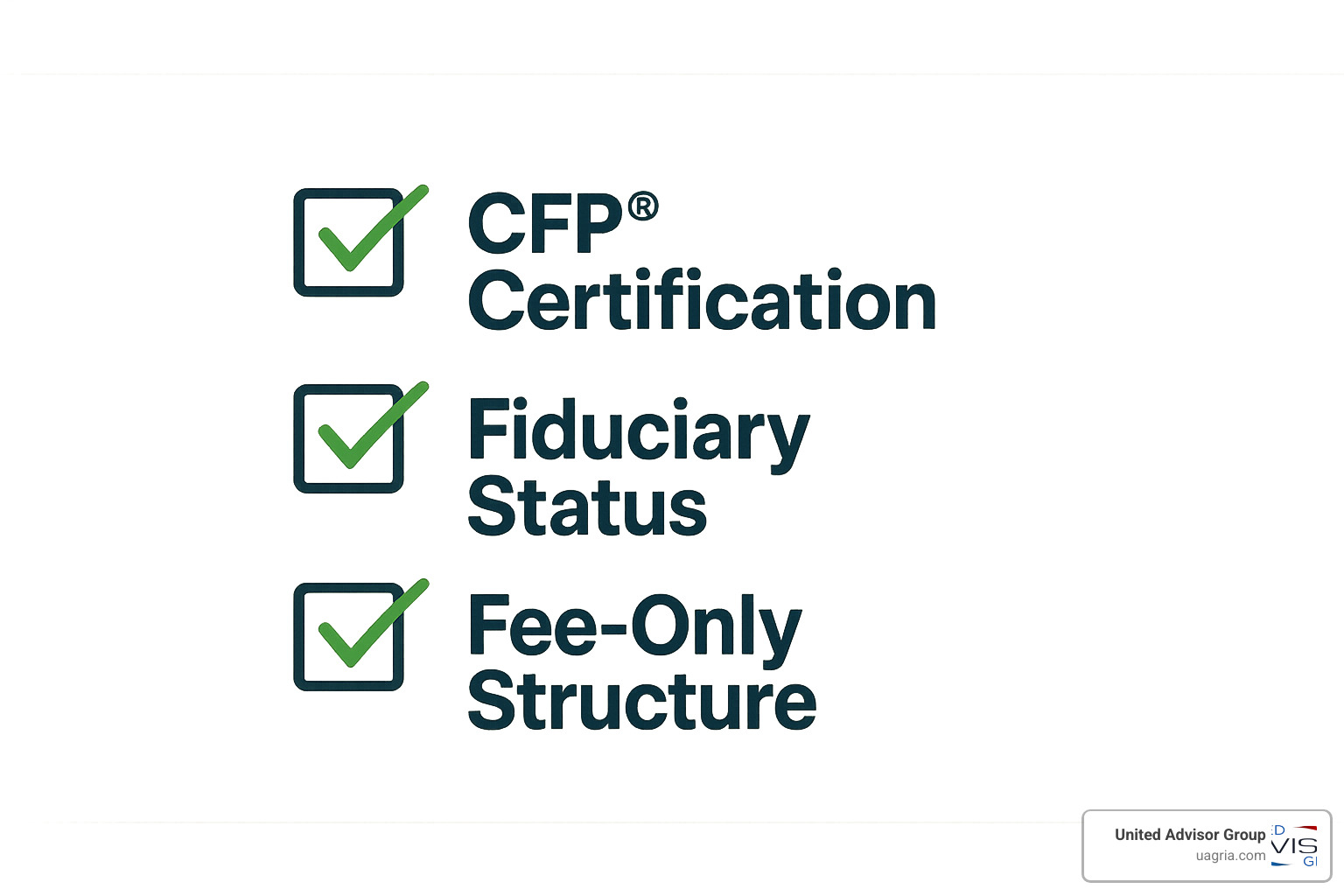

- Look for credentials: CFP®, CPA with PFS, RICP®, or EA designations

- Verify fiduciary status: Ensure they’re legally bound to act in your best interest

- Understand fee structure: Fee-only advisors offer the most transparent pricing

- Check specialization: Retirement tax planning requires specific expertise beyond general financial advice

- Consider virtual options: Many top advisors now serve clients nationwide through technology

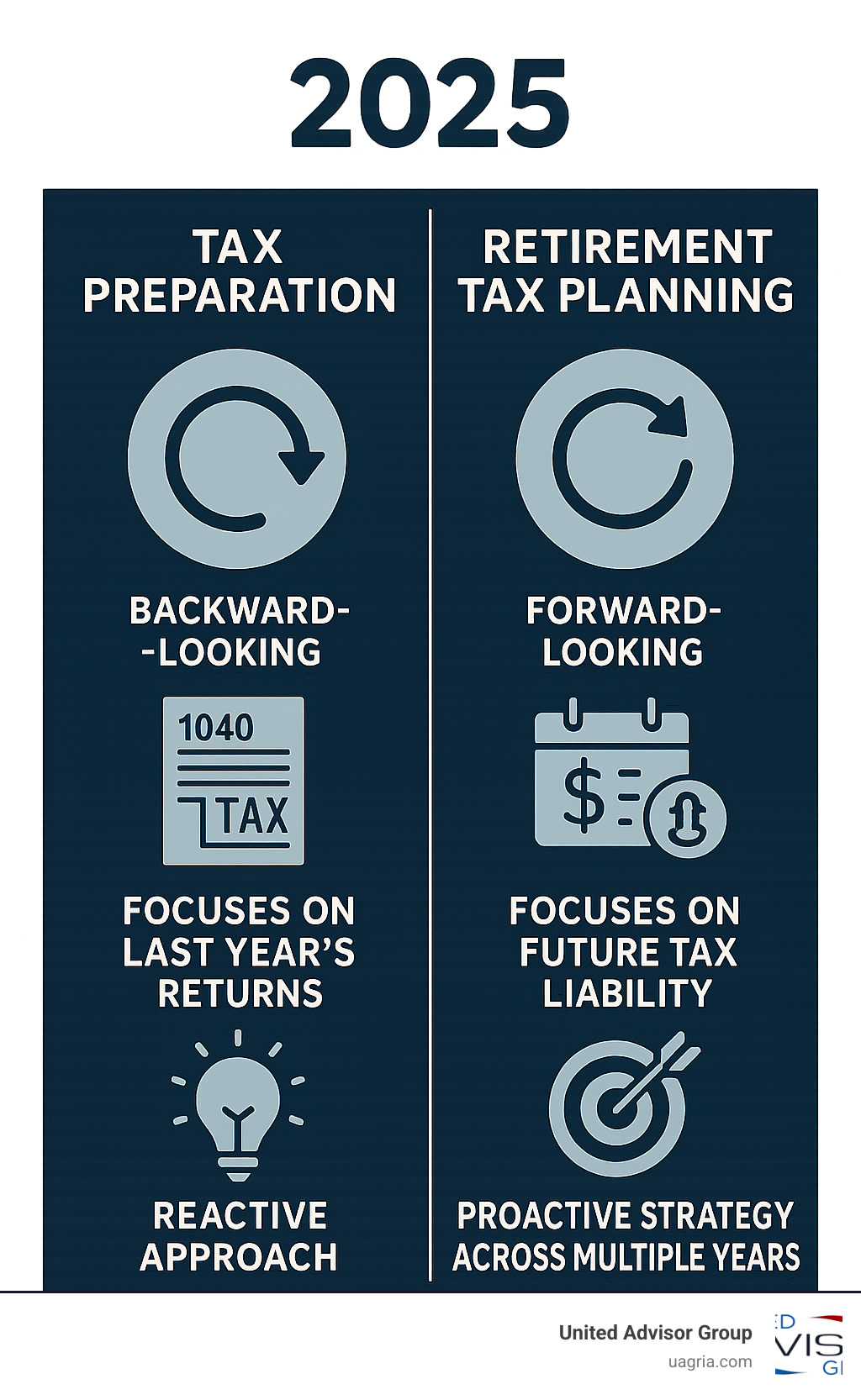

The reality is stark: taxes can be your biggest expense in retirement. Without proper planning, you could pay thousands more than necessary or accidentally push yourself into higher tax brackets. A specialized retirement tax planning advisor focuses on minimizing your future tax liability, not just filing last year’s returns.

This isn’t about basic tax preparation – it’s about creating a comprehensive strategy that coordinates your Social Security benefits, manages Required Minimum Distributions (RMDs), and optimizes withdrawal timing across different account types. The best advisors understand that retirement planning is fundamentally different from accumulation planning.

As Ray Gettins, Director of United Advisor Group, I’ve seen how independent advisors can transform retirement outcomes when they’re free from proprietary product pressures and compliance burdens. My experience helping elite advisors serve their clients better has shown me that finding the right retirement tax planning advisor near me often means looking beyond traditional broker-dealer models to truly independent professionals.

Why Specialization in Retirement Taxes Matters

Many people assume they’ll be in a lower tax bracket in retirement – but this isn’t always true. With traditional retirement accounts like 401(k)s and IRAs, you’re essentially in partnership with the IRS. They get their cut when you withdraw, and without proper planning, that cut can be substantial.

A specialized retirement tax planning advisor understands the complex interplay between:

- Multiple income streams: Social Security, pensions, retirement account withdrawals, and investment income all have different tax implications

- Required Minimum Distributions (RMDs): Starting at age 73, you must withdraw from traditional retirement accounts whether you need the money or not

- Tax bracket management: Strategic timing of withdrawals can keep you in lower brackets

- Healthcare costs: Medicare premiums increase with income, creating hidden tax penalties

- State tax considerations: Some states tax retirement income differently than others

The research shows that many tax advisors focus primarily on current-year tax reduction, but retirement tax planning requires a completely different approach. We need to look at your entire retirement timeline and project what your tax situation could look like throughout those years.

Common misconceptions include believing that:

- You’ll automatically be in a lower tax bracket in retirement

- Social Security benefits aren’t taxable

- All retirement accounts are taxed the same way

- Tax planning is only for the wealthy

A qualified Retirement and Tax Planning specialist knows these assumptions can be costly mistakes.

The Fiduciary Standard: Your Financial Guardian

When searching for a retirement tax planning advisor near me, the fiduciary standard should be non-negotiable. A fiduciary is legally obligated to act in your best interest at all times – not just when it’s convenient or profitable for them.

This matters because:

- No hidden commissions: Fiduciary advisors don’t earn money by selling you products

- Transparent advice: They must disclose any conflicts of interest

- Your interests first: Every recommendation must benefit you, not their bottom line

- Legal accountability: They can be held legally responsible for advice that isn’t in your best interest

The difference between a fiduciary and a non-fiduciary advisor can cost you thousands of dollars over your retirement. Non-fiduciary advisors only need to meet a “suitability” standard – meaning their recommendations just need to be suitable, not necessarily the best option for you.

At United Advisor Group, we champion Independent Financial Advice because we’ve seen how advisor autonomy leads to better client outcomes. When advisors aren’t pressured to sell proprietary products or meet sales quotas, they can focus entirely on what’s best for their clients.

How to Find a Qualified Retirement Tax Planning Advisor Near Me

Finding the right retirement tax planning advisor near me feels overwhelming at first, but breaking it down into manageable steps makes the process much clearer. The good news? Technology has opened up possibilities that didn’t exist even five years ago.

Your search should start with online directories that specialize in qualified advisors. The National Association of Personal Financial Advisors (NAPFA) maintains a comprehensive directory of fee-only, fiduciary advisors who’ve met strict educational and ethical requirements. Similarly, the CFP Board’s website allows you to search for Certified Financial Planners by location and specialty – a powerful tool when you need someone who truly understands retirement tax strategies.

Professional networks often yield the best referrals. Your current CPA likely knows financial planners who specialize in retirement tax planning, and this connection can be invaluable since they already understand your tax situation. Estate planning attorneys also work closely with financial advisors and can recommend professionals who understand the tax implications of retirement and legacy planning.

Don’t overlook virtual advisors in your search. Many top-tier retirement tax specialists now serve clients nationwide through secure video conferencing and digital document sharing. This approach can actually expand your options significantly, especially if you live in a smaller market where specialized expertise might be limited.

When it comes to referrals from friends and family, use them as a starting point rather than the final answer. Your neighbor’s advisor might be excellent for accumulation planning but lack the specialized knowledge needed for retirement tax strategies. Every situation is unique, and what works for someone else might not be the best fit for your specific needs.

Due diligence is crucial regardless of how you find potential advisors. Plan to interview at least three candidates, and don’t be afraid to ask detailed questions about their experience, credentials, and approach to retirement tax planning.

What to Look for in a Retirement Tax Planning Advisor Near Me

When evaluating potential advisors, credentials matter more than charm. The financial planning industry has varying levels of education and expertise, and you need someone with the right qualifications for retirement tax planning specifically.

The Certified Financial Planner (CFP®) designation represents the gold standard in comprehensive financial planning. These professionals complete extensive coursework, pass a rigorous exam, and maintain ongoing education requirements. Only about one-fourth of all financial advisors hold this designation, which tells you something about its value. Learn about the CFP designation to understand the demanding requirements these professionals must meet.

For retirement tax planning specifically, look for a Certified Public Accountant (CPA) with the Personal Financial Specialist (PFS) credential. This combination provides deep tax expertise alongside financial planning knowledge – exactly what you need for complex retirement tax strategies.

The Retirement Income Certified Professional (RICP®) designation focuses specifically on retirement income strategies, including tax-efficient withdrawal planning and Social Security optimization. This credential demonstrates specialized knowledge in the exact area you need help with.

Enrolled Agents (EAs) are licensed to represent taxpayers before the IRS and specialize in tax matters. While they might not provide comprehensive financial planning, they bring valuable tax expertise to retirement planning discussions.

Red flags should immediately eliminate potential advisors from consideration. Anyone who won’t clearly explain their fee structure, guarantees specific investment returns, or pushes proprietary products isn’t acting in your best interest. Similarly, advisors who don’t ask detailed questions about your situation or can’t explain their investment philosophy in plain English should be avoided.

NAPFA membership requires 60 hours of continuing education every two years, and less than 4% of financial planners qualify. This organization’s standards are among the highest in the industry, making membership a strong indicator of professional commitment.

Understanding Fee Structures: What Does ‘Fee-Only’ Really Mean?

The way your advisor gets paid directly impacts the advice you receive, making this one of the most important factors in your decision. Unfortunately, fee structures can be confusing, with terms like “fee-only” and “fee-based” sounding similar but meaning very different things.

Fee-only advisors are paid directly by clients only, through hourly rates, flat fees, or a percentage of assets under management. This structure eliminates most conflicts of interest because they don’t earn commissions from product sales or receive compensation from third parties. Their advice is based solely on what’s best for you, not what generates the highest fees for them.

Fee-based advisors use a combination of client fees and commissions, creating moderate conflicts of interest. While they might provide good advice, they may favor products that pay commissions. This doesn’t automatically make them bad advisors, but you need to understand these potential conflicts when evaluating their recommendations.

Commission-only advisors are paid exclusively through product sales, creating the highest potential for conflicts of interest. They’re incentivized to sell products rather than provide comprehensive planning, which generally makes them unsuitable for retirement tax planning.

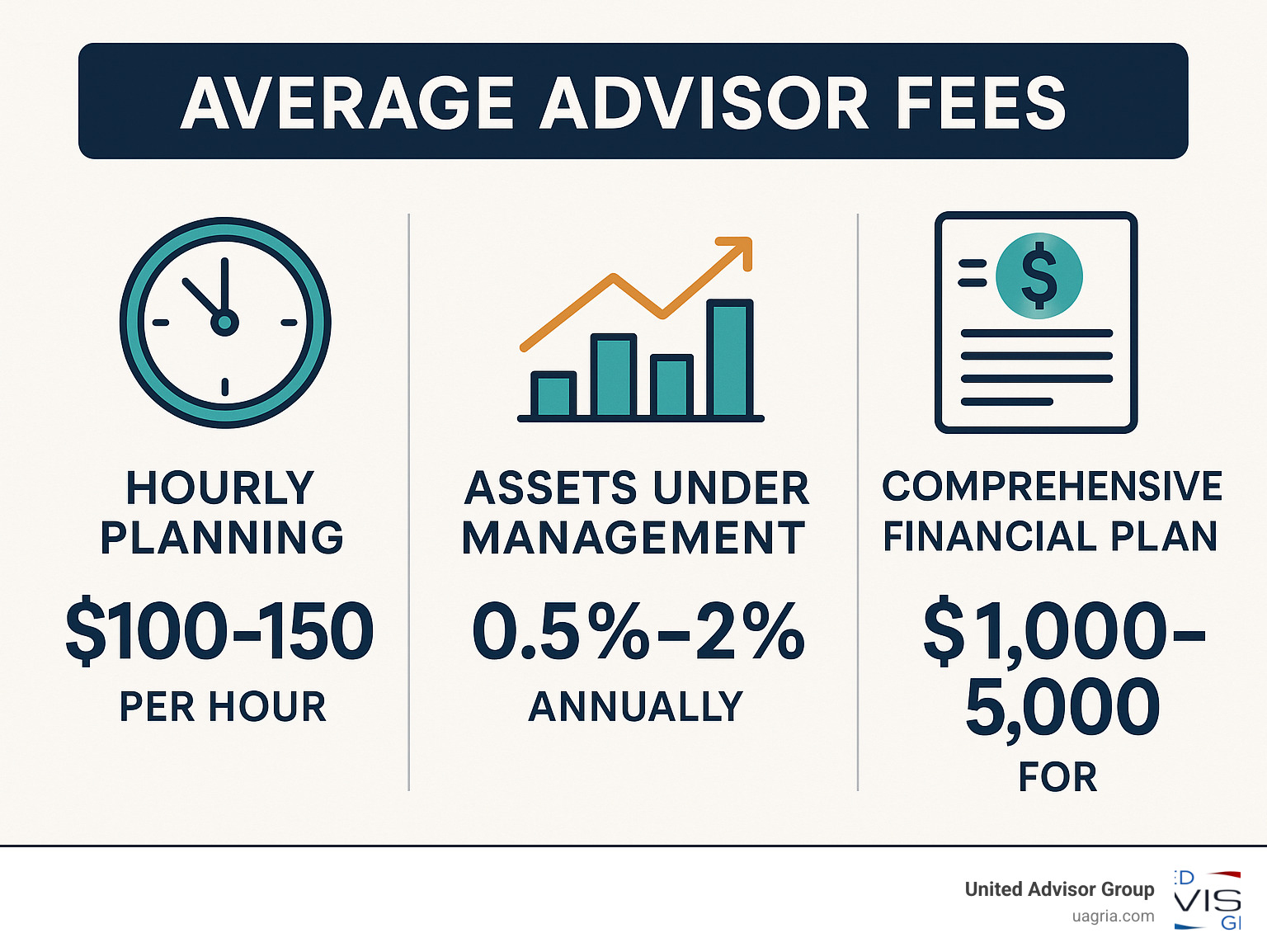

Research shows that financial planners typically charge $100-$150 per hour, with rates ranging from $45-$200 depending on experience and location. Some advisors charge flat annual fees or a percentage of assets under management instead of hourly rates.

Fee-only advisors are considered the gold standard because their compensation structure aligns with client interests. What is Fee-Only Advising? provides additional details on why this structure benefits clients.

At United Advisor Group, we support advisors who prioritize transparent fee structures because we’ve seen how this leads to better client outcomes. When advisors aren’t pressured by commission structures, they can focus on providing truly objective guidance through our Services.

Core Services: How an Advisor Minimizes Your Retirement Tax Bill

A qualified retirement tax planning advisor doesn’t just help you file taxes – they architect a comprehensive strategy to minimize your lifetime tax burden. The goal is to help you keep more of your hard-earned money throughout retirement.

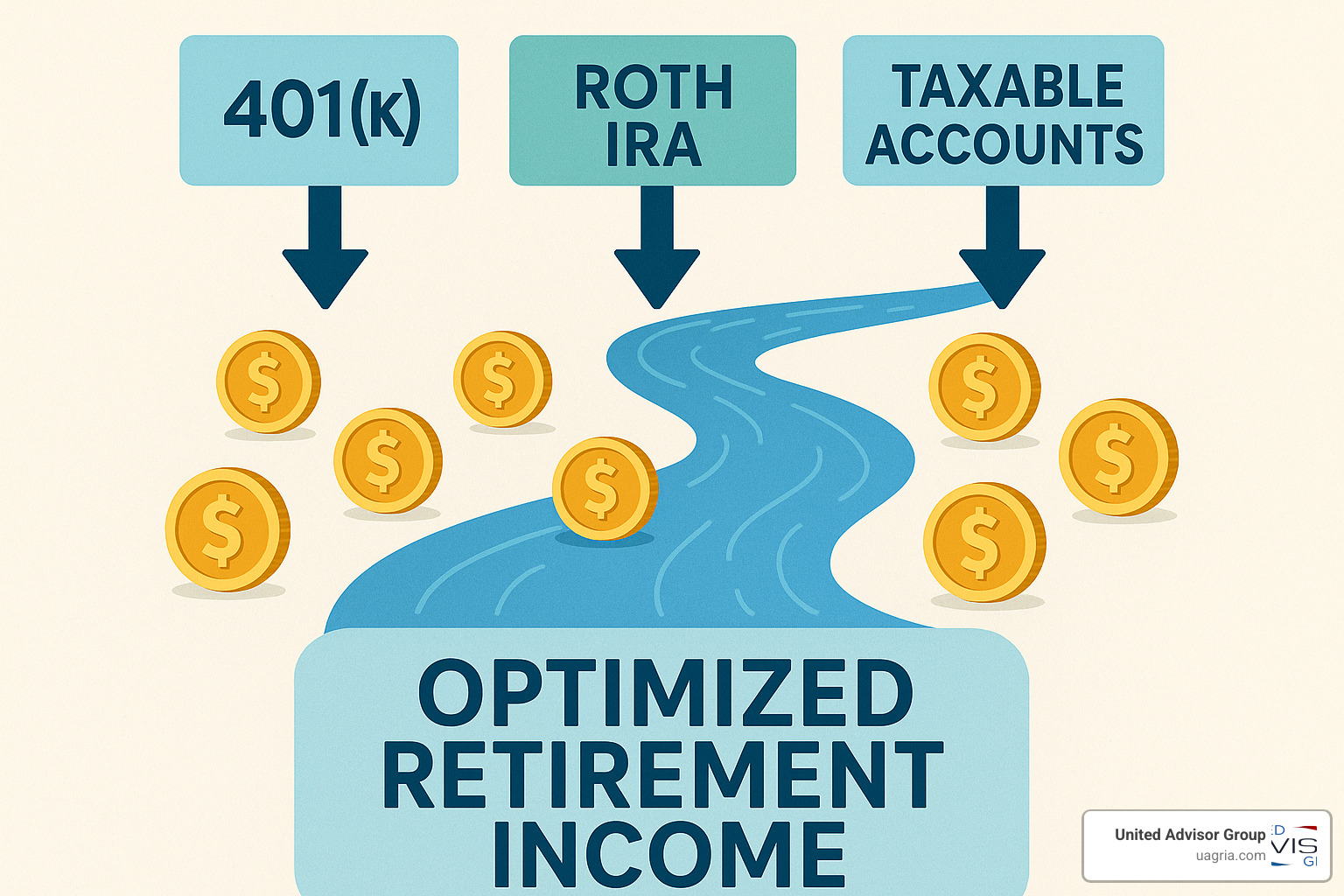

The key insight is understanding that you likely have money in three different “tax buckets”:

- Taxable accounts: You pay taxes on gains and dividends annually

- Tax-deferred accounts: Traditional 401(k)s and IRAs where you pay taxes on withdrawals

- Tax-free accounts: Roth IRAs and Roth 401(k)s where qualified withdrawals are tax-free

Strategic planning involves coordinating withdrawals from these different buckets to minimize your overall tax burden. This is where specialized expertise becomes crucial – the wrong withdrawal strategy can push you into higher tax brackets or trigger additional taxes on Social Security benefits.

Our research shows that with careful tax planning, some retirees can pay a 15% tax rate even while living a lifestyle that would normally put them in a 25% bracket. This level of tax efficiency requires sophisticated planning that goes far beyond basic tax preparation.

For business owners and those with complex financial situations, strategies like Open up Tax Savings with Financial Planning: IRC 1202 Tips can provide additional opportunities for tax optimization.

Strategic Tax Planning Services Offered

A comprehensive retirement tax planning advisor should offer these core services:

Roth Conversion Strategies: Converting traditional IRA or 401(k) assets to Roth IRAs can reduce future tax obligations. The key is timing these conversions during lower-income years to minimize the tax impact while creating tax-free income for later.

Tax-Loss Harvesting: Strategically realizing investment losses to offset gains and reduce taxable income. This technique can be particularly valuable in taxable investment accounts.

Asset Location Optimization: Placing different types of investments in the most tax-efficient accounts. For example, keeping tax-inefficient investments in tax-deferred accounts and tax-efficient investments in taxable accounts.

Qualified Charitable Distributions (QCDs): For those 70½ and older, making charitable donations directly from IRAs can satisfy RMD requirements while reducing taxable income.

RMD Management: Developing strategies to minimize the tax impact of Required Minimum Distributions, including timing of other withdrawals and potential Roth conversions before RMDs begin.

Social Security Optimization: Coordinating the timing of Social Security benefits with other income sources to minimize taxes on benefits and maximize lifetime income.

Estate and Gift Tax Planning: Implementing strategies to transfer wealth efficiently to heirs while minimizing estate and gift taxes.

Healthcare Cost Planning: Understanding how Medicare premiums increase with income and planning withdrawals to minimize these additional costs.

The Typical Process of Working with an Advisor

Understanding what to expect when working with a retirement tax planning advisor helps you evaluate whether they’re thorough and professional:

Initial Consultation (Usually complimentary): The advisor should ask detailed questions about your financial situation, retirement goals, risk tolerance, and tax concerns. They should explain their process and fee structure clearly.

Data Gathering: You’ll provide financial statements, tax returns, insurance policies, estate planning documents, and other relevant information. A thorough advisor will request at least three years of tax returns to understand your tax patterns.

Goal Setting and Analysis: The advisor will help you clarify your retirement goals and analyze your current financial position. They should project your retirement income needs and identify potential tax issues.

Strategy Development: Based on your situation, they’ll develop a comprehensive tax-efficient retirement plan. This should include specific recommendations for account management, withdrawal strategies, and tax optimization techniques.

Plan Presentation: You’ll receive a detailed written plan explaining their recommendations, including projections showing how different strategies impact your taxes and retirement security.

Implementation: The advisor will help you implement the recommended strategies, which might involve opening new accounts, making investment changes, or coordinating with other professionals.

Ongoing Monitoring: Regular reviews (typically quarterly or semi-annually) to monitor progress, adjust strategies based on tax law changes, and ensure you stay on track for your goals.

Annual Tax Planning: Year-end reviews to implement tax-saving strategies before December 31st and coordinate with your tax preparation.

Vetting Your Advisor: The Essential Questions to Ask

Think of this as the most important job interview you’ll ever conduct – except you’re the one doing the hiring. Finding the right retirement tax planning advisor near me isn’t just about impressive credentials or a fancy office. It’s about finding someone who genuinely understands your situation and can explain complex tax strategies in plain English.

I’ve seen too many people rush into advisor relationships because they felt pressured or didn’t want to seem “difficult” by asking tough questions. Don’t make that mistake. A good advisor will welcome your questions and take time to answer them thoroughly.

You’re potentially entering a relationship that could last decades and significantly impact your financial security. The advisor who gets annoyed by your questions isn’t the right fit. The one who lights up when discussing tax strategies and asks follow-up questions about your specific situation? That’s your person.

At United Advisor Group, we’ve learned that the best client relationships start with complete transparency. Independent advisors who aren’t tied to proprietary products can afford to be completely honest about their approach, fees, and limitations.

Key Questions to Ask a Potential Retirement Tax Planning Advisor Near Me

The conversation should feel natural, but make sure you cover these crucial areas. Don’t be afraid to take notes – any advisor worth their salt will appreciate that you’re taking this seriously.

Start with the fiduciary question – it’s that important. Ask directly: “Are you a fiduciary, and will you put that in writing?” If they hem and haw or give you a complicated answer, that’s a red flag. A true fiduciary will say yes immediately and explain what that means for you.

Money talk comes next, and it should be crystal clear. Ask them to break down exactly how they’re compensated. Do they charge hourly fees? A percentage of your assets? Are there any commissions involved? The best advisors will hand you a fee schedule and walk through it line by line.

Here’s a question that separates the pros from the pretenders: “Do you receive any compensation from third parties for recommending products?” If the answer is yes, that doesn’t automatically disqualify them, but you need to understand exactly what those arrangements are.

Their credentials matter, but don’t just accept alphabet soup after their name. Ask when they earned their certifications and what continuing education they complete. A CFP® designation earned 20 years ago isn’t as valuable if they haven’t kept up with changes in tax law.

Get specific about their approach to retirement tax planning. Can they explain their philosophy on Roth conversions? How do they coordinate with your existing CPA? Do they have experience with clients in situations similar to yours?

Ask about their typical client – this tells you a lot. If you’re a teacher with a modest 403(b) and they usually work with executives who have millions in stock options, you might not get the attention you deserve.

The communication question is crucial: How often will you meet? Do they prefer phone calls, video conferences, or in-person meetings? What happens if you have questions between scheduled meetings?

Don’t forget to ask “What happens if you retire or leave the business?” It’s an uncomfortable question, but you need to know if there’s a succession plan or if you’ll be left scrambling to find a new advisor.

For additional insights on this vetting process, check out Key Considerations for Selecting a Financial Advisor in D.C. – the principles apply no matter where you live.

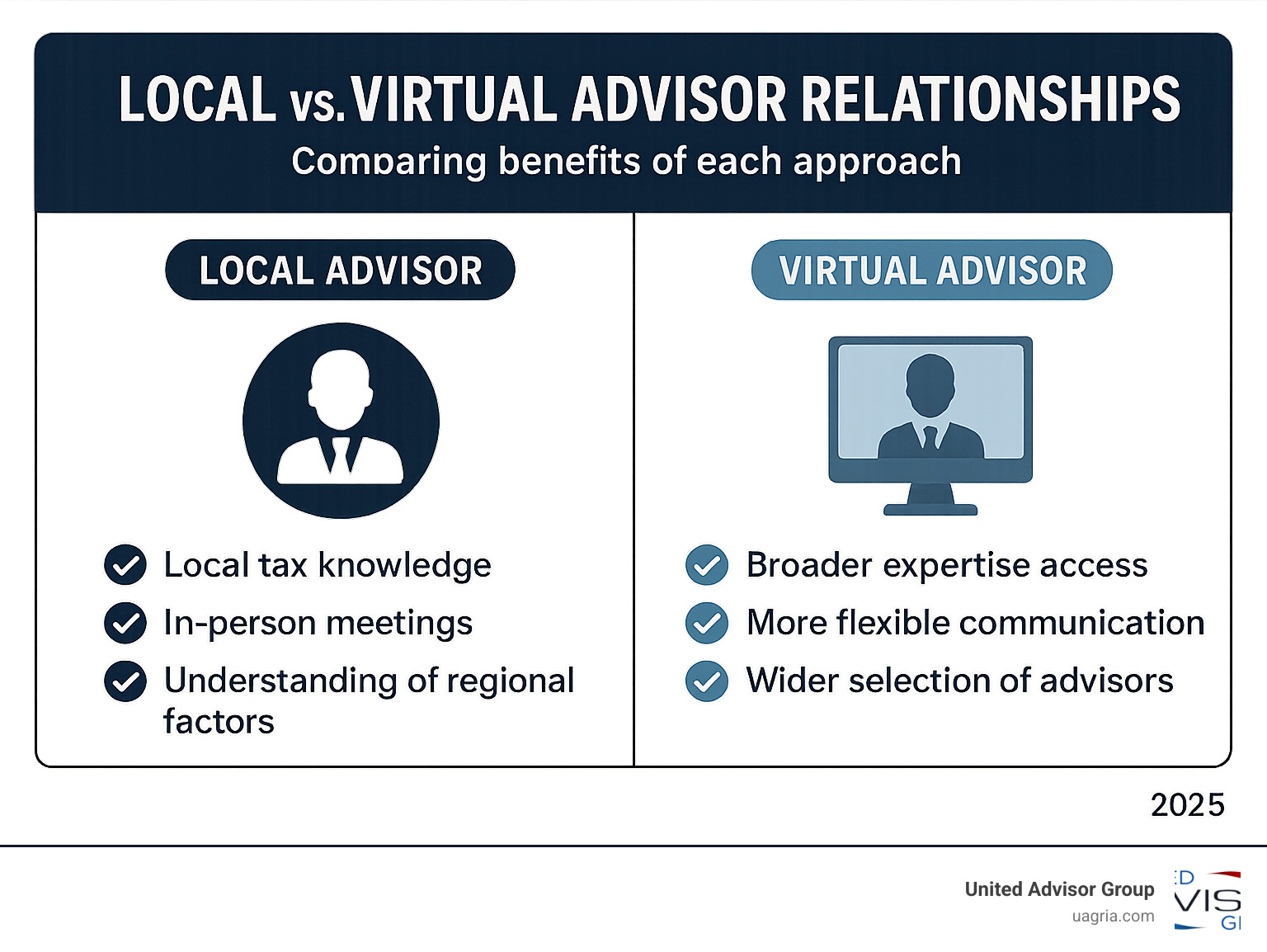

The “Near Me” Debate: Does Location Still Matter?

Here’s where things get interesting. The whole concept of finding a retirement tax planning advisor near me has evolved dramatically. Your best advisor might be three time zones away, and that could actually work in your favor.

Location still matters in some situations. If you live in a state with quirky tax laws – think California’s complex rules or New York’s various tax complications – having an advisor who deals with these issues daily can be valuable. Some people simply prefer face-to-face meetings, especially when discussing something as personal as their financial future.

But here’s the reality: most retirement tax planning involves federal tax law, which is the same whether you’re in Maine or Arizona. The strategies for managing RMDs, optimizing Social Security benefits, and coordinating tax-efficient withdrawals work the same way nationwide.

Technology has changed everything. I’ve watched advisors conduct incredibly effective client meetings via video conference, share documents instantly through secure portals, and provide real-time portfolio updates. Some clients tell me they actually prefer virtual meetings because they can review documents on their own computer screen rather than squinting at papers across a desk.

Think about it this way: would you rather work with a mediocre advisor who’s 15 minutes away, or an exceptional specialist who’s 1,500 miles away but available via video call? The answer seems obvious when you put it like that.

The key is finding someone who understands your specific needs, regardless of their zip code. As we explore in Is Location the Best Factor for Choosing a Wealth Manager?, the advisor’s expertise and approach matter far more than their physical location.

Virtual relationships offer some real advantages. You get access to specialists who might not be available in your local market. You can often get more flexible meeting times. And there’s something to be said for an advisor who isn’t tied to your local social or business networks – they can give you completely objective advice.

The bottom line? Don’t limit yourself geographically if it means settling for less expertise or a poor fit. The right advisor who serves you virtually will provide better results than a mediocre advisor who’s located nearby.

Conclusion: Secure Your Financial Future with the Right Partner

Finding the right retirement tax planning advisor near me is honestly one of the most important financial decisions you’ll make. I’ve seen too many people struggle in retirement simply because they didn’t get the right tax planning help early enough.

Here’s the reality: taxes can quietly eat away at your retirement savings for decades. But here’s the good news – with proper planning, you can significantly reduce that burden. We’ve worked with advisors whose clients save thousands of dollars annually through smart tax strategies. Over a 20-30 year retirement, those savings really add up.

The key is finding an advisor who truly puts your interests first. Look for someone who operates as a fiduciary – they’re legally bound to act in your best interest, not their own. This matters more than you might think. When advisors aren’t pressured to sell specific products or meet sales quotas, they can focus entirely on what’s best for you.

Credentials matter, but so does specialization. A CFP® or CPA with PFS designation shows they’ve done the work to understand complex financial planning. But make sure they actually specialize in retirement tax planning, not just general financial advice. There’s a big difference between someone who helps you accumulate wealth and someone who helps you keep it during retirement.

Don’t get hung up on location. The best advisor for your situation might not be in your neighborhood, and that’s perfectly fine. Technology has made virtual relationships incredibly effective. What matters is finding someone who understands your specific needs and can explain complex concepts in plain English.

At United Advisor Group, we’ve built our entire mission around supporting independent advisors who can provide truly objective, client-focused advice. When advisors are free from proprietary product pressures and broker-dealer compliance burdens, they can focus entirely on what’s best for their clients. That’s the kind of advisor you want in your corner.

Your ideal advisor should be someone who takes time to understand your unique situation. They should provide written projections showing exactly how their strategies will impact your taxes. They should coordinate with your CPA and attorney. Most importantly, they should communicate in a way that makes sense to you.

This isn’t just about finding someone to manage your investments. You’re looking for a strategic partner who will help you steer the complex intersection of taxes, investments, and retirement income planning. The right advisor becomes an invaluable part of your financial team.

Your retirement security is too important to leave to chance. Take the time to interview multiple candidates. Ask the tough questions about their credentials, fee structure, and approach. Trust your instincts about communication style and expertise.

Start your search today for a qualified retirement tax planning advisor who will put your interests first and help you build the tax-efficient retirement you deserve. For additional resources and to learn more about our approach to independent financial advice, visit our Trusted Financial Planner Services in Dayton, Ohio page or Contact Us directly.

The right partnership can make all the difference in your retirement years. Take that next step – your future self will thank you for it.