The Rise of Independent Advisor Firms: Your Path to Unbiased Financial Guidance

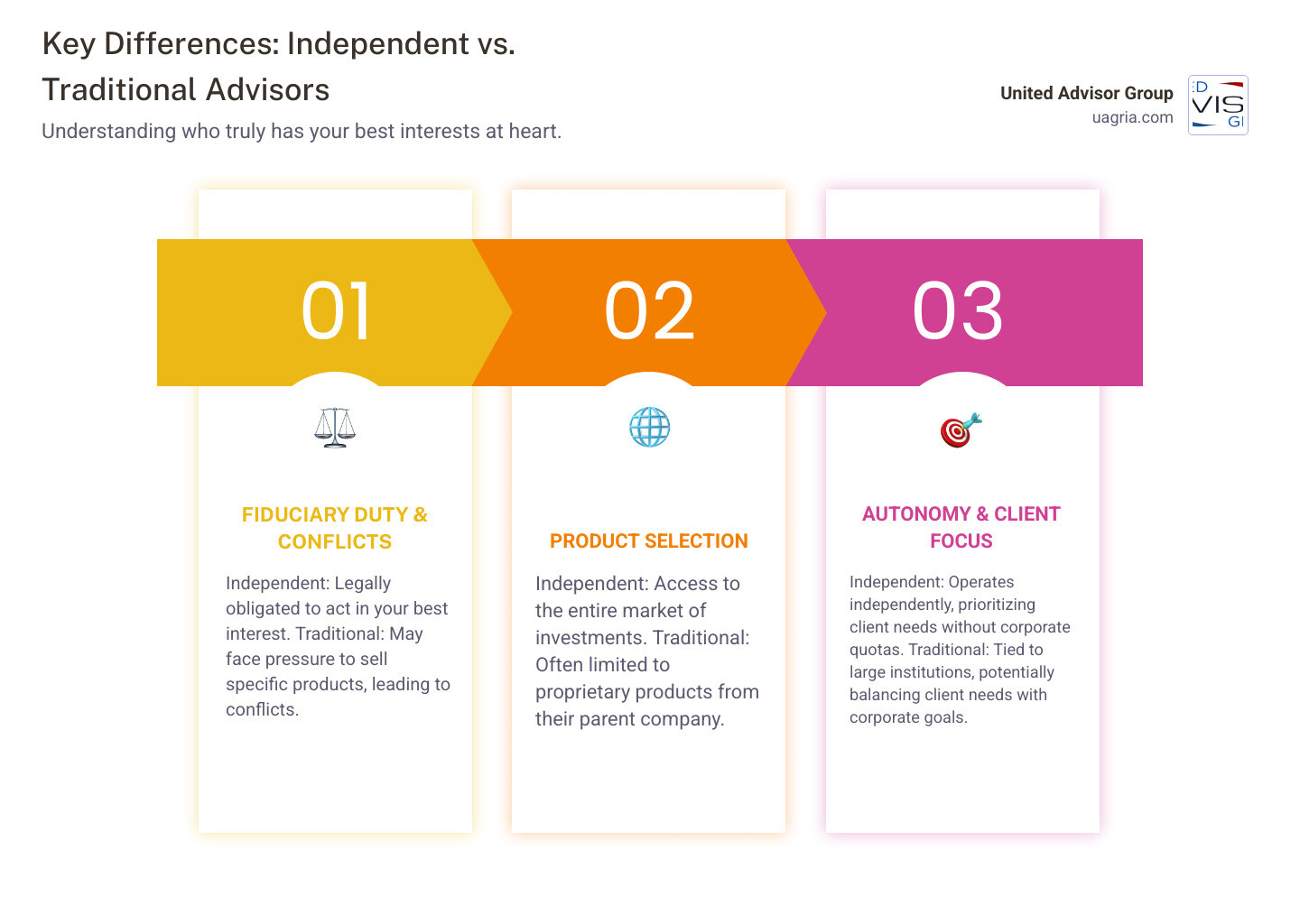

Independent advisor firms are financial advisory practices that operate independently, meaning they are not owned by or tied to a larger bank, brokerage, or financial product provider. This structure often allows them to offer unbiased advice and prioritize client needs without the conflicts of interest found in traditional institutions.

Key characteristics often include:

- Autonomy: They have the freedom to choose from a vast array of investments and strategies. There’s no pressure to sell specific proprietary products.

- Client Focus: Their primary allegiance is to their clients, not a corporate parent. This leads to highly personalized service.

- Unbiased Advice: Because they are not constrained by internal product lists, they can offer objective recommendations custom to your unique situation.

- Fiduciary Standard: Many operate under a fiduciary duty, a legal requirement to always act in your best financial interest.

In today’s financial landscape, Americans want more than just advice—they want a trusted partner to help them achieve their financial goals. According to a recent survey, over 77 percent of Americans feel uncertain about their financial future. This highlights a clear and growing need for expert guidance. But not just any guidance. People are looking for advice they can truly trust.

This is where independent advisor firms step in. These firms represent a powerful shift in the financial industry. They offer a refreshing approach to managing your wealth, focusing squarely on your needs and aspirations. Unlike traditional financial institutions, independent firms are built on freedom and flexibility. This means they can put your interests first, every single time.

I’m Ray Gettins, Director at United Advisor Group. Our group is built by advisors for advisors, and we focus on empowering independent advisor firms to better serve their clients through collaboration and extensive resources.

What is an Independent Advisor Firm?

Have you ever wondered what truly sets some financial advisors apart? An independent advisor firm is a financial advisory business that operates free from bank, wire-house, or insurance-company ownership. Because they are not tied to a parent company, independent firms can draw from the entire marketplace instead of a short, proprietary menu. This autonomy makes it far easier to put your interests first.

Many of these businesses register as a Registered Investment Advisor (RIA), which legally obligates them to act as a fiduciary—always putting the client’s best interest ahead of their own. That single distinction underpins the “client-first” culture most people seek when they look for truly Independent Financial Advice.

How They Differ from Other Advisory Models

Traditional brokerage and bank advisors often work inside a sales culture—budgets, quotas, and house products usually come with the territory. Independent advisor firms take the opposite approach. They keep products at arm’s length and let planning lead the conversation. Because many firms are owned by the very advisors you meet with, there’s a built-in sense of accountability and an entrepreneurial drive to keep service personal. Learn more about the power of No Proprietary Products.

The Rise of the Independent Model

Independence is no longer a niche. Advisors have migrated away from the big brands in record numbers, taking more than $5 trillion of client assets with them. The resulting “mega-RIAs” prove that independence can scale, delivering Wall-Street-level resources without Wall-Street conflicts.

The Core Benefits of Working with an Independent Advisor

Choosing an independent advisor firm gives you something many investors never experience—unbiased, personalized guidance delivered by someone whose livelihood depends on your long-term success, not short-term commissions.

Top 5 Advantages for Clients

- Fiduciary Commitment – RIAs must legally act in your best interest.

- Objective Advice – No sales quotas, no house products.

- Customized Planning – Strategies built around your life, not the average client.

- Greater Transparency – Clear fees, straightforward reports.

- Direct Accountability – Often you work with the owners themselves.

Why the Fiduciary Standard is a Game-Changer

Brokers follow a “suitability” rule; fiduciaries follow a “best-interest” rule. That extra legal duty removes the gray area and aligns advisor success with your success—delivering peace of mind that every recommendation is made for you, not for a payout. For deeper context, see how independent advisors support fiduciary virtual family office roles.

Services and Compensation of Independent Advisor Firms

An independent firm acts like a financial “general contractor,” coordinating every part of your plan:

- Comprehensive financial planning – budgeting, goal mapping, cash-flow projections

- Investment management – portfolio design, implementation, oversight

- Retirement planning – savings targets, income strategies, longevity analysis

- Estate planning – coordinating with attorneys so assets pass as intended

- Tax strategies – integrating tax-smart investing and distribution tactics

- Insurance review – objective assessment of coverage and costs

Find the full menu of services.

Understanding the ‘Fee-Only’ Compensation Model

“Fee-only” means the client pays the advisor—period. No product commissions, no hidden trails. Common structures include:

- AUM percentage – typically around 1 % and declines on larger balances

- Flat or project fees – fixed cost for a defined scope of work

- Hourly or retainer – ideal for targeted advice without large asset minimums

Because compensation rises only when the client prospers, incentives stay aligned.

TABLE comparing Fee-Only vs. Commission-Based Compensation

| Feature | Fee-Only Independent Advisor | Commission-Based Advisor |

|---|---|---|

| Compensation Source | Directly from the client (AUM %, flat fee, hourly) | Commissions from selling financial products |

| Potential Conflict | Minimized; advice is the product | Higher; incentive to sell commission-based products |

| Product Selection | Open architecture; access to entire market | May be limited to certain products |

| Transparency | High; fees are clearly disclosed | Can be lower; commissions may be embedded in product costs |

How to Choose a Reputable Independent Advisor Firm

Finding the right partner is much like hiring any professional—check credentials, review work samples, and verify there are no skeletons in the regulatory closet.

Key Steps in Your Vetting Process

- Clarify your goals. Know whether you need full-service planning, investment help, or a one-time project.

- Seek referrals. Ask friends, attorneys, or CPAs whom they trust.

- Interview at least three firms. First meetings are usually complimentary—use them.

- Request a sample plan. Quality firms happily provide anonymized examples.

- Verify credentials and history. Look for CFP®, CFA, or similar marks and run a quick check on the SEC’s free Investment Adviser Public Disclosure database or FINRA’s BrokerCheck tool to confirm licenses and view any disciplinary records.

When comparing options, see how each firm fits the wealth manager vs. financial advisor spectrum.

Understanding a Firm’s Form ADV and Form CRS

- Form ADV – the long-form filing that spells out services offered, exact fees, disciplinary events, and conflicts of interest. Firms are required to provide this document to prospective clients.

- Form CRS – a two-page summary in plainer language, perfect for quick comparisons. This relationship summary is also a required disclosure.

Spend 10 minutes with these documents and you’ll know more than most investors ever will before they hire an advisor.

The Future of Financial Advice: Technology and Trends

Technology has levelled the playing field: small independent advisor firms can now access the same research, trading, and planning tools once reserved for Wall Street.

How Technology Empowers Independent Advisor Firms

- Digital portals – 24/7 access to performance, documents, and secure messaging

- Advanced planning software – real-time scenario modeling for “what-if” decisions

- Automation – routine tasks like rebalancing or reporting executed in the background

- Robust cybersecurity – bank-level encryption and multi-factor authentication

These efficiencies have driven the cost of planning tools down by 90 %, savings that flow straight to clients.

Current Industry Trends and Future Outlook

- Mega-RIAs – large independents prove that scale and objectivity can coexist

- Specialization – niche experts for tech professionals, physicians, entrepreneurs, and more

- Holistic advice – integrating taxes, estate, and insurance under one roof

- Hyper-personalization – data analytics tailor portfolios and plans to each household

Advisors continue to seek independence because, as outlined in What growth-minded investment advisors aim to achieve, autonomy lets them focus squarely on the client. Expect even more innovation as technology and the independent model evolve together.

Frequently Asked Questions about Independent Advisors

We understand you might have more questions as you explore independent advisor firms. It’s completely natural to want all the details before making such an important decision! Here are some common questions we hear, and our straightforward answers.

Are independent advisors more expensive than other advisors?

This is a fantastic question, and the answer might surprise you! Not necessarily, and often, choosing an independent advisor firm can actually be more cost-effective in the long run. Why? It comes down to transparency and alignment of interests.

When you work with an independent, fee-only advisor, their fees are typically very clear and paid directly by you. Think of it like paying a doctor or a lawyer—you know exactly what their time and expertise cost. This contrasts sharply with models where advisors earn commissions from selling specific products. Those commissions might make the advice seem “free,” but they’re often hidden within product costs, sales charges, or higher expense ratios on proprietary funds. With an independent advisor firm, you’re paying for objective advice, not a sales pitch. Their success is tied directly to your financial success, creating a powerful alignment that can ultimately save you money by avoiding high-commission products and ensuring your plan is truly in your best interest.

What is the difference between an independent advisor and a Registered Investment Advisor (RIA)?

This can definitely be a bit confusing, as these terms are often used interchangeably. But let’s clear up the nuance!

An independent advisor describes the business structure and philosophy of a firm. It means the advisor or firm operates autonomously, not tied to a larger bank, brokerage, or financial product provider. They have the freedom to choose from a vast universe of investments and strategies, always prioritizing their clients’ needs without corporate pressure. It’s about their independence in serving you.

A Registered Investment Advisor (RIA), on the other hand, is a legal and regulatory designation. It means the firm or individual providing investment advice for compensation is formally registered with either the Securities and Exchange Commission (SEC) or relevant state securities regulators. The key takeaway here is that RIAs are held to a fiduciary standard, meaning they are legally obligated to always act in your best financial interest.

So, while most independent advisor firms operate as RIAs because this structure allows them to uphold that crucial fiduciary duty, the term “independent” highlights their business model and client-first philosophy, whereas “RIA” refers to their formal legal status and higher standard of care.

How much money do I need to work with an independent advisor?

This is another common concern, and it’s great news that the answer is: it varies widely, and there’s likely an independent advisor firm that fits your situation!

While some larger, highly ranked independent firms might have minimums starting in the high six figures or even millions of dollars, many others are much more accessible. The independent space is incredibly diverse, and you’ll find a wide range of service models.

For example, many independent firms offer lower asset minimums or provide different service tiers to accommodate various financial situations. Even better, a growing number of independent advisors offer hourly consulting or project-based financial planning for a set fee. This is a fantastic option if you don’t meet traditional asset minimums but need specific, expert guidance on a particular financial goal, like creating a retirement plan or optimizing your budget. The independent model is all about flexibility and client focus, making quality financial advice increasingly accessible. Don’t hesitate to ask about their minimums and alternative service options during your initial consultations – you might be surprised by the possibilities!

Conclusion: Taking Control of Your Financial Future

Your financial future doesn’t have to feel uncertain or overwhelming. Throughout this guide, we’ve explored how independent advisor firms offer a refreshing alternative to traditional financial institutions. These firms bring something special to the table: genuine freedom to put your interests first, every single time.

The key benefits we’ve discussed aren’t just marketing points—they’re real advantages that can transform your financial journey. When you work with an independent firm, you get unbiased advice because there are no proprietary products to push. You receive personalized strategies because your advisor has the flexibility to craft solutions just for you. Most importantly, you gain a true partner who’s legally bound by the fiduciary standard to act in your best interest.

This fiduciary commitment isn’t just a nice-to-have feature. It’s a game-changer that provides genuine peace of mind. When your advisor is legally required to put your financial well-being above their own profits, you can trust that every recommendation serves your goals, not their sales targets.

The financial advisory industry is evolving rapidly, and independent advisor firms are leading this positive change. They’re leveraging technology to provide better service at lower costs, while maintaining the personal touch that makes all the difference. As more advisors choose independence and more clients demand transparency, this model continues to grow stronger.

At United Advisor Group, we’ve built our entire philosophy around supporting advisor autonomy because we know it leads to better outcomes for you. When advisors have the freedom to operate without proprietary product pressures or unnecessary compliance burdens, they can focus on what truly matters: your financial success and peace of mind.

Taking control of your financial future means making informed choices about who you trust with your wealth. By choosing an independent advisor firm, you’re not just hiring someone to manage your money—you’re gaining a committed partner who will stand by you through market ups and downs, life changes, and evolving goals.

Your financial journey is unique, and you deserve advice that reflects that. Seek out an independent advisor who will listen to your dreams, understand your concerns, and work tirelessly to help you achieve both. This partnership approach, built on trust and shared success, is what will ultimately improve your client relationships with a registered investment advisor and create the secure financial future you’re working toward.

The power to choose is in your hands. Make it count.