Why Building a Long-Term Financial Plan is Your Path to True Financial Freedom

How to make a long term financial plan starts with understanding that financial freedom isn’t about quick wins or market timing – it’s about creating a systematic approach that grows your wealth over decades. Here’s the essential framework:

9-Step Long-Term Financial Planning Process:

- Assess your current financial health – Calculate net worth and track cash flow

- Set SMART financial goals – Define specific, measurable targets with timelines

- Create a purposeful budget – Use the 50/30/20 rule for needs, wants, and savings

- Build an emergency fund – Save 3-6 months of living expenses

- Eliminate high-interest debt – Use snowball or avalanche methods

- Develop an investment strategy – Diversify across asset classes based on risk tolerance

- Plan for retirement – Maximize tax-advantaged accounts and employer matches

- Manage risks and taxes – Secure appropriate insurance and optimize tax strategies

- Review and adjust regularly – Schedule annual check-ups and milestone celebrations

The research shows that Americans who have a written financial plan feel more in control of their finances compared to those without one. Yet over half of adults lack even three months of emergency savings, and the average household carries more than $104,000 in debt.

Long-term planning works because of compound growth and disciplined habits. A carefully planned approach can extend your portfolio’s longevity by more than three years on average, while consistent saving of just 10-15% of post-tax income can secure your retirement decades ahead.

As Ray Gettins, Director at United Advisor Group, I’ve spent years helping advisors understand how to make a long term financial plan that truly serves their clients’ best interests. My experience has shown that the most successful financial plans prioritize client outcomes over product sales, which is why collaboration and independence matter so much in this process.

Why Long-Term Financial Planning Matters

Long-term financial planning is the process of projecting your financial situation over multiple years or decades to achieve specific life goals. Unlike short-term planning that focuses on immediate needs (typically 1-2 years), long-term planning extends 5, 10, or even 30+ years into the future.

The importance of this extended timeline cannot be overstated. According to the Government Finance Officers Association, organizations should maintain financial plans that project at least five years into the future, and the same principle applies to personal finance. This horizon allows you to:

- Harness the power of compound growth – Time is your greatest asset when building wealth

- Weather market volatility – Short-term fluctuations become less significant over decades

- Make strategic decisions – You can plan major life events like home purchases, education funding, and retirement

- Build financial confidence – Research shows people with written plans feel more in control of their finances

The confidence factor is particularly important. A 2024 Charles Schwab survey found that people who engage in financial planning feel significantly more confident about their financial future than those who don’t. This isn’t just about having more money – it’s about having a clear roadmap that reduces anxiety and enables better decision-making.

Compound growth is perhaps the most compelling reason to start long-term planning early. When you consistently save and invest over decades, your money doesn’t just grow – it accelerates. The returns on your investments begin generating their own returns, creating a snowball effect that becomes increasingly powerful over time.

Consider this: if you save $200 monthly starting at age 25, assuming a 7% annual return, you’ll have over $500,000 by age 65. Wait until age 35 to start, and you’ll have less than $250,000. That 10-year delay costs you more than $250,000 – demonstrating why we often say “it’s not timing the market; it’s time in the market.”

How to Make a Long Term Financial Plan: Step-by-Step Blueprint

Creating a comprehensive long-term financial plan might seem overwhelming, but breaking it into manageable steps makes the process achievable. We’ve developed a proven 9-step framework that addresses every aspect of your financial life, from your current situation to your future dreams.

This systematic approach ensures you don’t miss critical elements while building a plan that adapts to your changing circumstances. Each step builds upon the previous one, creating a solid foundation for long-term financial success.

How to Make a Long Term Financial Plan: Assess Your Current Financial Health

Before charting your course to financial freedom, you need to know exactly where you stand today. This assessment forms the foundation of your entire plan and helps identify both opportunities and challenges ahead.

Calculate Your Net Worth

Your net worth is the difference between what you own (assets) and what you owe (liabilities). This single number provides a snapshot of your financial health and serves as a baseline for measuring progress.

Assets include:

- Cash and savings accounts

- Investment accounts (401k, IRA, brokerage)

- Real estate equity

- Personal property (vehicles, valuable items)

- Business interests

Liabilities include:

- Mortgage balances

- Credit card debt

- Student loans

- Auto loans

- Personal loans

Don’t be discouraged if your net worth is negative – this is common, especially for younger adults with student loans. The key is understanding your starting point and tracking improvement over time.

Track Your Cash Flow

Understanding your monthly income and expenses is crucial for identifying how much you can allocate toward your long-term goals. Track everything for at least three months to get an accurate picture.

Income sources might include:

- Primary employment salary

- Side business income

- Investment dividends

- Rental property income

- Other regular income streams

Expenses typically fall into two categories:

- Fixed expenses (rent, insurance, minimum debt payments)

- Variable expenses (groceries, entertainment, discretionary spending)

Monitor Your Credit Score

Your credit score affects your ability to borrow money and the interest rates you’ll pay. Higher scores mean lower borrowing costs, which can save thousands over time. Check your credit report regularly and address any inaccuracies promptly.

Understanding your current financial health enables you to make informed decisions about goal setting and resource allocation. This assessment also helps identify areas for immediate improvement, such as reducing unnecessary expenses or addressing high-interest debt.

For those seeking guidance through this process, collaborative financial planning can provide valuable insights and accountability.

How to Make a Long Term Financial Plan: Set Clear & Achievable Goals

Goal setting transforms abstract financial dreams into concrete, actionable targets. Without clear goals, even the best financial habits lack direction and purpose.

Use the SMART Framework

SMART goals are Specific, Measurable, Achievable, Relevant, and Time-bound. This framework ensures your goals are clear and trackable.

Instead of “I want to save for retirement,” a SMART goal would be: “I will save $500,000 for retirement by age 60 by contributing $1,000 monthly to my 401k and IRA accounts.”

Categorize Your Goals by Timeline

- Short-term goals (1-2 years): Emergency fund, debt payoff, vacation savings

- Medium-term goals (3-10 years): Home down payment, education funding, major purchases

- Long-term goals (10+ years): Retirement, children’s college education, legacy wealth

Distinguish Needs from Wants

Prioritize goals based on necessity versus desire. Needs include emergency funds, adequate insurance, and retirement savings. Wants might include luxury vacations or expensive hobbies. Both are valid, but needs should take priority in your resource allocation.

Create Milestone Mapping

Break large goals into smaller, manageable milestones. If you’re saving $50,000 for a home down payment over five years, your milestones might be:

- Year 1: Save $10,000

- Year 2: Save $20,000 total

- Year 3: Save $30,000 total

- Year 4: Save $40,000 total

- Year 5: Reach $50,000 goal

This approach makes large goals feel achievable and provides regular opportunities to celebrate progress.

Consider using a financial goals worksheet to organize and track your objectives systematically.

Build a Purposeful Budget & Robust Emergency Fund

A well-structured budget serves as the engine that powers your long-term financial plan. It ensures you’re consistently allocating resources toward your goals while maintaining your current lifestyle.

The 50/30/20 Rule

This simple framework provides a starting point for budget allocation:

- 50% for needs: Housing, utilities, minimum debt payments, groceries, transportation

- 30% for wants: Entertainment, dining out, hobbies, non-essential purchases

- 20% for savings and debt payoff: Emergency fund, retirement contributions, extra debt payments

Adjust these percentages based on your specific situation. If you have high-interest debt, you might allocate more than 20% to debt elimination temporarily.

Separate Fixed from Discretionary Expenses

Fixed expenses remain relatively constant each month (rent, insurance, loan payments), while discretionary expenses vary (entertainment, shopping, dining out). Understanding this distinction helps identify areas where you can reduce spending to fund your goals.

Automate Your Success

Set up automatic transfers to savings and investment accounts immediately after each paycheck. This “pay yourself first” approach ensures your goals get funded before discretionary spending can interfere.

Build Your Emergency Fund

Your emergency fund serves as financial insurance, protecting you from unexpected expenses without derailing your long-term plans. Experts recommend saving three to six months of living expenses, though the exact amount depends on your situation.

Consider a larger emergency fund if you:

- Have irregular income

- Work in an unstable industry

- Have dependents

- Own a home

- Have limited insurance coverage

Start with a smaller goal if six months seems overwhelming. Even $500 can prevent you from using credit cards for minor emergencies. Build gradually by automating small, consistent transfers.

Keep your emergency fund in a separate, easily accessible account to avoid the temptation to spend it on non-emergencies. High-yield savings accounts offer better returns than traditional savings while maintaining liquidity.

Tame and Eliminate Debt for Long-Term Success

High-interest debt acts like a weight dragging down your financial progress. The average American household carries over $104,000 in debt, including mortgages and credit cards. While some debt (like mortgages) can be beneficial, high-interest consumer debt should be eliminated as quickly as possible.

Choose Your Debt Elimination Strategy

Debt Snowball Method: Pay minimums on all debts while putting extra money toward the smallest balance. Once paid off, roll that payment into the next smallest debt. This method provides psychological wins that maintain motivation.

Debt Avalanche Method: Pay minimums on all debts while putting extra money toward the highest interest rate debt. This method saves more money in interest charges over time.

Both methods work – choose based on your personality. If you need motivation and quick wins, use the snowball. If you’re disciplined and want to minimize interest costs, use the avalanche.

Follow the 28/36 Guideline

This rule suggests spending no more than 28% of your gross monthly income on housing costs and no more than 36% on total debt payments. Staying within these limits helps ensure you can handle your debt obligations while still saving for the future.

Consider Debt Consolidation

If you have multiple high-interest debts, consolidation might lower your overall interest rate and simplify payments. Options include:

- Balance transfer credit cards (often with 0% introductory rates)

- Personal loans with lower rates than credit cards

- Home equity loans (if you own a home)

Be cautious with consolidation – it only works if you avoid accumulating new debt on the paid-off accounts.

Monitor Your Progress

Use tools like the Credit Karma app to track your credit score improvement as you pay down debt. Seeing your score increase provides additional motivation to stay on track.

Eliminating debt isn’t just about the math – it’s about freeing up cash flow for your long-term goals and reducing financial stress.

Investing & Retirement Strategies for Decades of Growth

Once you’ve built your emergency fund and eliminated high-interest debt, investing becomes your primary wealth-building tool. The key to long-term investment success isn’t timing the market or finding the next hot stock – it’s consistent contributions to a diversified portfolio aligned with your risk tolerance and timeline.

Understanding Asset Allocation

Asset allocation – how you divide your investments among stocks, bonds, and other assets – is the most important investment decision you’ll make. Your allocation should reflect your:

- Time horizon: Longer timelines allow for more aggressive growth investments

- Risk tolerance: Your comfort level with market volatility

- Financial goals: Different objectives may require different strategies

A common rule of thumb suggests subtracting your age from 100 to determine your stock allocation percentage. A 30-year-old might hold 70% stocks and 30% bonds, while a 60-year-old might prefer 40% stocks and 60% bonds.

ETFs vs. Mutual Funds

Exchange-traded funds (ETFs) have become increasingly popular for long-term investors because they offer:

- Lower expense ratios than most mutual funds

- Greater tax efficiency

- Daily transparency of holdings

- No minimum investment requirements

However, mutual funds still have advantages, including professional management and automatic dividend reinvestment. The choice depends on your preferences and investment approach.

Maximize Retirement Accounts

Tax-advantaged retirement accounts are powerful wealth-building tools. For 2025, contribution limits are:

- 401(k): $23,500 (plus $7,500 catch-up for ages 50+)

- IRA: $7,000 (plus $1,000 catch-up for ages 50+)

- Special catch-up: Ages 60-63 can contribute an additional $11,250 to 401(k)s

Always contribute enough to your 401(k) to capture the full employer match – it’s free money that can significantly boost your retirement savings.

Plan for Longevity

Life expectancy data shows that a 30-year-old male can expect to live 45.34 more years, while a 30-year-old female can expect 50.38 more years. Your retirement savings need to last potentially 20-30 years or more after you stop working.

This longevity risk makes it crucial to:

- Start saving early to maximize compound growth

- Maintain some growth investments even in retirement

- Plan for healthcare costs, which typically increase with age

- Consider inflation’s impact over decades

Diversification and Risk Management

Don’t put all your eggs in one basket. Diversify across:

- Asset classes: Stocks, bonds, real estate, commodities

- Geographic regions: Domestic and international markets

- Company sizes: Large-cap, mid-cap, and small-cap stocks

- Sectors: Technology, healthcare, financials, etc.

Regular rebalancing ensures your portfolio stays aligned with your target allocation as market movements shift your percentages.

For personalized investment strategies that align with your specific goals and risk tolerance, consider exploring custom investment solutions that prioritize your interests over product sales.

Risk Management, Taxes & Estate Planning Essentials

Protecting your wealth is just as important as building it. A comprehensive long-term financial plan addresses potential risks that could derail your progress and optimizes your tax efficiency to keep more of what you earn.

Essential Insurance Coverage

Insurance protects against catastrophic financial losses that could destroy years of careful planning. Consider these key types:

Health Insurance: Medical expenses are a leading cause of bankruptcy. Ensure you have adequate coverage, and consider a Health Savings Account (HSA) if eligible – it offers triple tax benefits.

Disability Insurance: One in four of today’s 20-year-olds will experience a work-limiting disability before retirement. Disability insurance replaces income if you can’t work due to illness or injury. Employer-provided coverage typically replaces about 60% of salary, so consider supplemental coverage.

Life Insurance: If others depend on your income, life insurance provides financial security for your family. Term life insurance offers affordable coverage for specific periods, while permanent life insurance combines coverage with investment features.

Property Insurance: Protect your home and belongings with adequate homeowners or renters insurance. Consider umbrella policies for additional liability protection.

Tax-Advantaged Account Strategies

Strategic use of tax-advantaged accounts can significantly impact your long-term wealth accumulation:

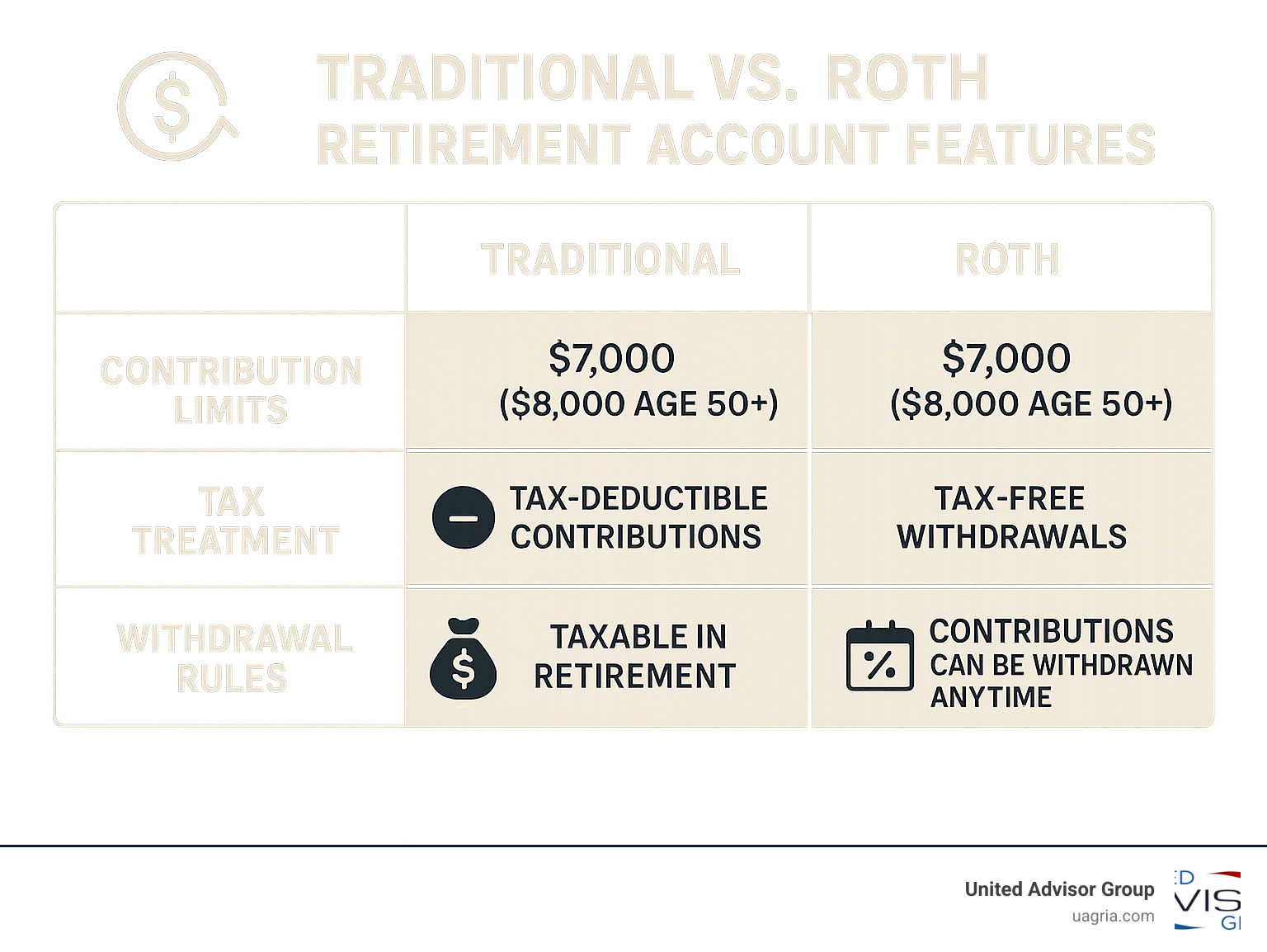

Traditional vs. Roth Accounts:

- Traditional: Contributions are tax-deductible now, but withdrawals in retirement are taxed

- Roth: Contributions are made with after-tax dollars, but qualified withdrawals are tax-free

The choice depends on whether you expect to be in a higher or lower tax bracket in retirement. Many investors use both types for tax diversification.

Health Savings Accounts (HSAs): Often called “super IRAs,” HSAs offer triple tax benefits:

- Tax-deductible contributions

- Tax-free growth

- Tax-free withdrawals for qualified medical expenses

After age 65, you can withdraw HSA funds for any purpose (paying taxes like a traditional IRA), making them excellent retirement vehicles.

Estate Planning Fundamentals

Estate planning ensures your assets transfer according to your wishes while minimizing taxes and legal complications. Essential documents include:

Will: Specifies how your assets should be distributed and names guardians for minor children.

Power of Attorney: Designates someone to make financial decisions if you become incapacitated.

Healthcare Directive: Outlines your medical care preferences and names someone to make healthcare decisions.

Beneficiary Designations: Keep these updated on all accounts – they supersede your will for retirement accounts and life insurance.

Trusts: May be beneficial for larger estates or specific situations like providing for disabled beneficiaries or minimizing estate taxes.

Withdrawal Strategies

Research shows that a carefully planned withdrawal strategy can add more than three years to a portfolio’s longevity. Consider:

- The 4% rule as a starting point (withdraw 4% of your portfolio value annually)

- Tax-efficient withdrawal sequencing

- Roth conversions during lower-income years

- Required minimum distributions from traditional accounts

For comprehensive guidance on optimizing your tax strategies and retirement planning, explore retirement and tax planning services that focus on your specific situation.

Reviewing, Adjusting & Staying Motivated Over the Years

A long-term financial plan isn’t a “set it and forget it” document. Life changes, markets fluctuate, and your goals evolve. Regular reviews and adjustments keep your plan relevant and effective.

Schedule Annual Financial Check-ups

Set a specific date each year to review your financial plan comprehensively. Many people choose their birthday or the beginning of the year. During this review:

- Calculate your current net worth and compare to previous years

- Assess progress toward each goal

- Rebalance investment portfolios

- Update insurance coverage

- Review and adjust budget allocations

- Consider tax-loss harvesting opportunities

Celebrate Milestones

Acknowledging progress maintains motivation for the long journey ahead. Celebrate when you:

- Reach net worth milestones

- Pay off debts

- Max out retirement contributions

- Build your emergency fund

- Achieve savings goals

Celebrations don’t need to be expensive – they just need to acknowledge your progress and reinforce positive financial behaviors.

Adapt to Life Changes

Major life events require plan adjustments:

- Marriage: Combine financial goals and strategies

- Children: Adjust for new expenses and education savings

- Career changes: Modify income projections and benefit strategies

- Inheritance: Integrate windfall into existing plans

- Health issues: Reassess insurance needs and timeline goals

Automate What You Can

Technology makes it easier to stick to your plan:

- Automatic transfers to savings and investment accounts

- Automatic bill payments to avoid late fees

- Rebalancing alerts from investment platforms

- Spending tracking through budgeting apps

Behavioral Finance Considerations

Understanding common psychological biases helps you make better financial decisions:

- Loss aversion: People feel losses more strongly than equivalent gains

- Recency bias: Recent events seem more important than they are

- Overconfidence: Overestimating your ability to predict market movements

- Analysis paralysis: Delaying decisions due to too many options

Recognizing these tendencies helps you stick to your long-term plan even when emotions suggest otherwise.

When to Seek Professional Help

Consider professional guidance when you:

- Have complex financial situations

- Lack time to manage investments

- Need accountability and motivation

- Face major life transitions

- Want specialized expertise in areas like tax planning or estate planning

The key is finding advisors who prioritize your interests over product sales. Independent financial advice can provide objective guidance without conflicts of interest from proprietary products.

Frequently Asked Questions about Long-Term Financial Plans

How often should I review my long-term financial plan?

We recommend conducting a comprehensive review annually, with quarterly check-ins to monitor progress and make minor adjustments. However, you should review your plan immediately after major life events such as marriage, divorce, job changes, inheritance, or health issues.

The annual review should include:

- Net worth calculation and progress tracking

- Goal reassessment and timeline adjustments

- Investment portfolio rebalancing

- Insurance coverage evaluation

- Tax strategy optimization

- Estate planning document updates

Quarterly reviews can be simpler, focusing on budget performance, savings rate, and any needed course corrections.

What size emergency fund do experts recommend?

Most financial experts recommend an emergency fund covering three to six months of essential living expenses. However, the right amount depends on your specific situation:

Three months may be sufficient if you have:

- Stable employment

- Dual-income household

- Good insurance coverage

- Limited dependents

Six months or more may be better if you have:

- Irregular income or commission-based work

- Single-income household

- Dependents

- Health issues

- Older home requiring maintenance

Your emergency fund should cover essential expenses only – not your entire current spending. Focus on housing, utilities, food, transportation, insurance, and minimum debt payments.

When is it wise to seek professional financial advice?

Consider professional guidance when you:

Have complex financial situations such as:

- Multiple income sources

- Business ownership

- Significant assets requiring tax planning

- Estate planning needs beyond basic documents

Lack time or expertise to:

- Research investment options

- Monitor portfolio performance

- Stay current with tax law changes

- Manage complex financial strategies

Need accountability and motivation to:

- Stick to your savings plan

- Avoid emotional investment decisions

- Maintain long-term perspective during market volatility

Face major life transitions including:

- Retirement planning

- Divorce or death of spouse

- Inheritance or windfall

- Career changes or business sale

The key is finding advisors who act as fiduciaries, putting your interests first rather than selling products for commissions.

Conclusion

Creating a successful long-term financial plan requires patience, discipline, and the right guidance. The nine-step framework we’ve outlined provides a comprehensive roadmap for building wealth over decades, but your plan should evolve as your life changes.

At United Advisor Group, we believe in putting your interests first. Our client-focused approach means we help advisors serve their clients without the pressure of proprietary products or broker-dealer compliance burdens. This independence allows for truly objective advice that prioritizes your financial success over product sales.

How to make a long term financial plan isn’t just about following steps – it’s about creating a sustainable system that adapts to your changing needs while keeping you focused on your long-term objectives. Whether you’re just starting your financial journey or looking to optimize an existing plan, the key is to begin today.

Financial freedom isn’t achieved overnight, but with consistent effort and the right strategy, it’s absolutely achievable. Start with step one – assessing your current financial health – and build momentum from there. Your future self will thank you for the discipline and foresight you demonstrate today.

For personalized guidance on implementing these strategies, consider exploring trusted financial planning services that prioritize your success over product sales. The journey to financial freedom begins with a single step, and there’s no better time to take that step than right now.